Michele Azzone, Carlo Bechi, Gabriele Sbaiz

1. Introduction

The increasing frequency, severity, and unpredictability of natural disasters and chronic climate threats pose unprecedented challenges to global financial markets. Traditional asset pricing models and portfolio management frameworks often struggle to incorporate the stochastic nature of physical climate risks.

Currently, investors attempting to hedge against physical climate risk often rely on static, country-level vulnerability indices or long-term macroeconomic projections. These approaches fail to capture the high-frequency, dynamic nature of extreme weather events and their heterogeneous impacts across different industries and individual firms. The motivation of this research is to bridge this gap by connecting firm-specific asset intensity with the time-varying probability of extreme temperature anomalies, ultimately allowing for dynamic risk mitigation within a quantitative portfolio construction paradigm.

The core hypothesis is that while market participants are increasingly aware of transition risks (e.g., regulatory changes, carbon taxes), the immediate and localized impacts of physical climate shocks—such as floods, extreme heatwaves, and storms—are not yet fully priced into global equity variations. Addressing this requires granular data and a departure from standard variance models.

3. Methodology

3.1. Panel Regression Analysis and Sectoral Impact

The foundation of the study is a robust panel regression analysis conducted on historical sectoral returns. We focus on extreme temperature events, formalizing them as localized temperature anomalies. By regressing sectoral equity returns against these anomalies, we provide strong statistical evidence that extreme temperature shocks exert a quantifiable negative effect on the majority of economic sectors. Notably, the empirical findings show statistically significant adverse impacts not only in traditionally exposed sectors like agriculture or industrials, but also in sectors such as Retailers and Software & IT Services, highlighting the widespread vulnerability of supply chains and technological infrastructure.

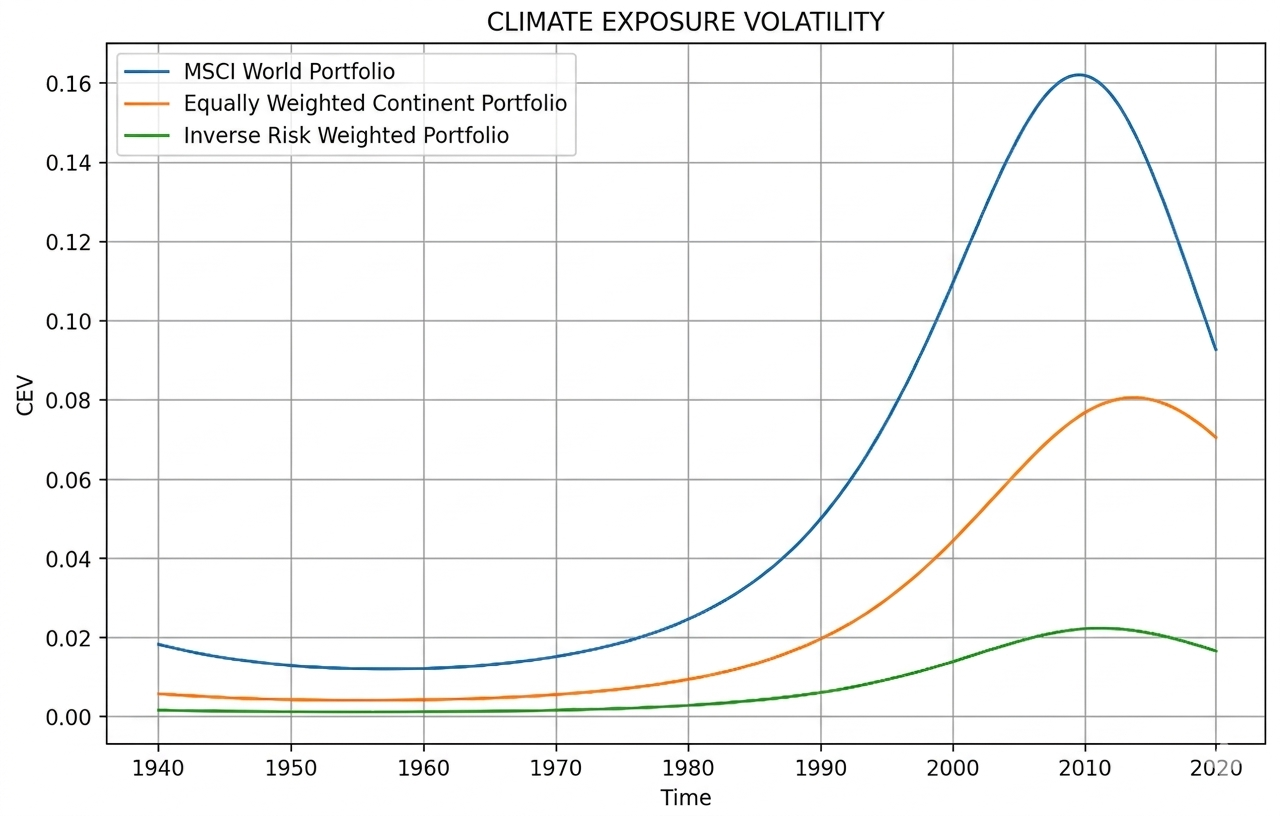

3.2. Novel Climate Risk Metrics: CRE and CEV

To operationalize these findings for portfolio optimization, we introduce two novel, dynamic metrics designed to measure the environmental vulnerability of an investment portfolio:

- Climate Risk Exposure (CRE): A measure of the expected impact of temperature anomalies on a portfolio, taking into account the firm-specific asset intensity and geographic distribution of operations. It represents the aggregate vulnerability of the portfolio to realized and expected physical climate shocks.

- Climate Exposure Volatility (CEV): A metric capturing the variance or uncertainty associated with the portfolio’s climate risk exposure. This highlights that climate risk is not static; the probability of extreme events varies over time, and CEV measures the stability of the portfolio’s climate resilience.

By utilizing realized temperature anomalies and multiplying them by climate-normalized asset weights, the metrics are aggregated geographically to produce a robust monthly indicator of risk. These indices provide a much more responsive tool compared to static ESG scores.

3.3. Multi-Objective Portfolio Optimization

The core contribution of the paper is the integration of CRE and CEV into a multi-objective portfolio optimization framework. This novel approach extends the classical Markowitz Mean-Variance paradigm by adding climate risk dimensions. Investors are no longer restricted to optimizing the trade-off between expected financial return and financial variance; they can now actively minimize Climate Exposure Volatility (CEV) or constrain Climate Risk Exposure (CRE). This allows for the construction of portfolios that are explicitly resilient to physical climate shocks while maintaining desired levels of financial diversification.

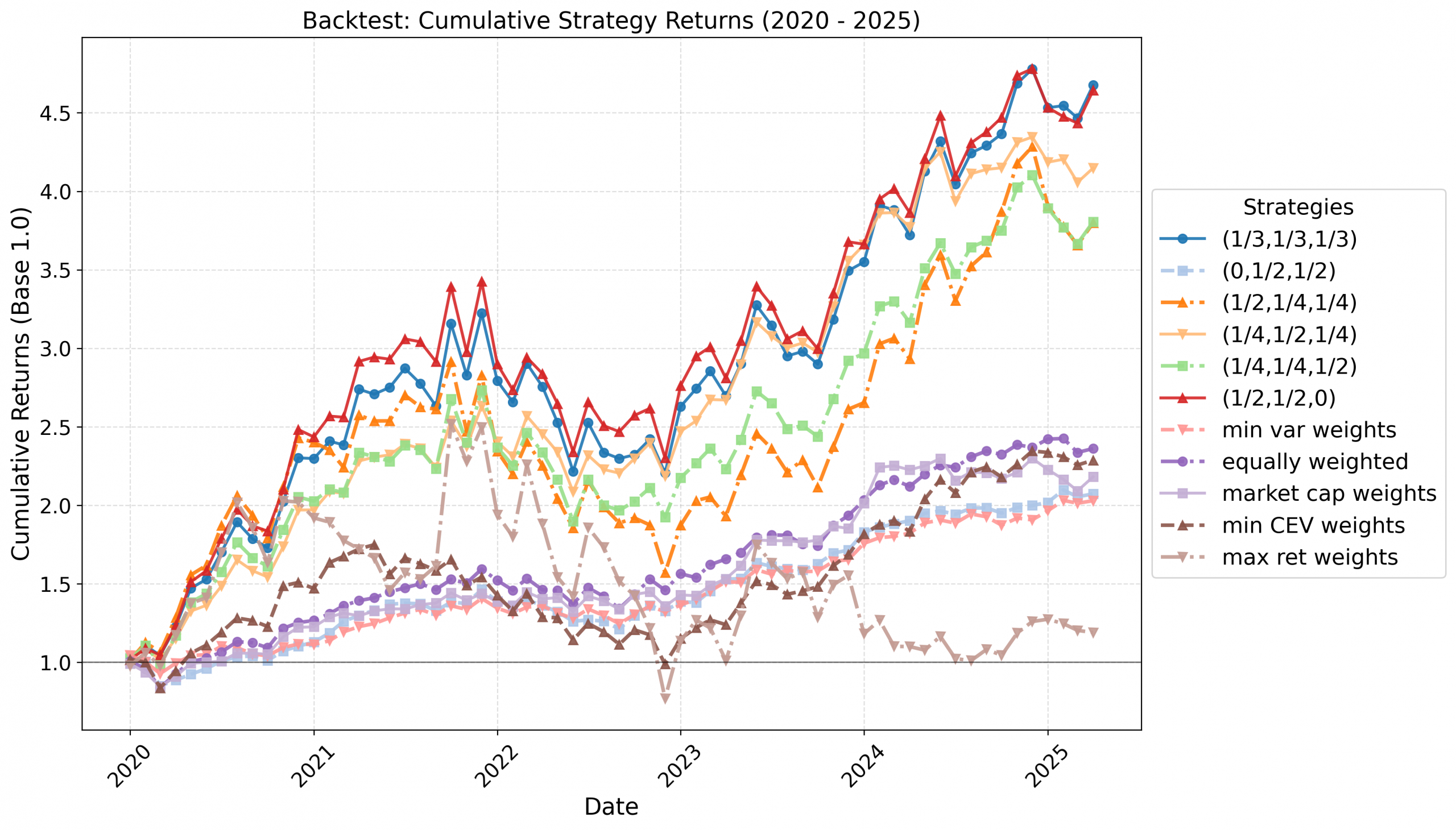

4. Backtesting

To show the practical benefits of the proposed methodology, we conduct an extensive backtesting analysis over the period from January 2020 to April 2025.

The study compares three distinct portfolio strategies to evaluate the trade-offs between traditional optimization and climate-aware frameworks. By plotting the evolution of CEV across these three strategies, we discuss how active management of climate risk exposure leads to superior resilience during periods of heightened climatic stress.

The out-of-sample performance metrics reveal that incorporating CRE and CEV into the investment process does not come at an unacceptable cost to financial returns. Instead, the climate-aware strategies perform competitively relative to traditional benchmarks, while offering significantly lower drawdown profiles during periods characterized by high global temperature anomalies and associated natural disasters. The inclusion of firm-specific physical footprints allows for highly targeted reallocations that preserve the core equity premium.

5. Conclusion

We provide a highly practical, statistically grounded methodology for addressing one of the most pressing risks in modern quantitative finance. By introducing dynamic, firm-level and temperature-driven metrics (CRE and CEV) and embedding them into a multi-objective optimization framework, we offer a blueprint for constructing resilient global equity portfolios. This approach empowers asset managers to systematically mitigate the adverse effects of physical climate risk, ensuring long-term portfolio stability without sacrificing the benefits of broad market diversification.

Link to the preprint: https://arxiv.org/abs/2604.11143