The European Banking Authority (EBA) published today its annual report on risks and vulnerabilities in the EU banking sector. The report is accompanied by the results of the EBA’s 2018 EU-wide transparency exercise, which provide detailed information, in a comparable and accessible format, for 130 banks across the EU. Overall, the EU banking sector has continued to benefit from the positive macroeconomic developments in most European countries, which contributed to the increase in lending, further strengthening of banks’ capital ratios and improvements in asset quality. Profitability remains low on average and has not yet reached sustainable levels.

Source: European Banking Authority (EBA)

Source: European Banking Authority (EBA)

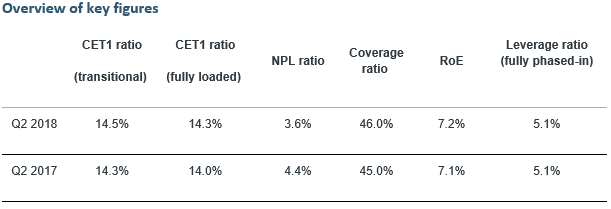

EU banks’ solvency ratios have increased, despite rising risk weighted assets (RWA) during the last two quarters. Since June 2017, CET1 ratios have increased from 14.3% to 14.5% on a transitional and from 14.0% to 14.3% on a fully loaded basis. The composition of capital keeps moving towards a greater reliance on retained earnings and other reserves.

Asset quality has further improved. The average NPL ratio of EU banks has decreased from 4.4% in June 2017 to 3.6% in June 2018. It has reached its lowest level since the NPL definition was harmonised across the EU in 2014, when it stood at 6.5%. NPL sales have contributed significantly to these reductions. However, vulnerabilities from downside risks to economic growth, revival of protectionism and elevated political risk remain high, which might jeopardise banks’ efforts to reduce legacy assets.

Profitability has virtually not changed since last year with an average return on equity (RoE) at 7.2% as of June 2018. EU banks’ net interest income has continued its declining trend in recent quarters, despite growing lending volumes, tightening the net interest margin further. Profitability has however benefited from the reduction of impairments and the increase of net fee and commission income. High costs and low efficiency represent a major driver of the poor performance of the EU banking sector. Costs dynamics are affected by elevated IT related expenses.

Despite increasing stable customer deposit funding, banks are facing key challenges on the liability side. Replacing financing from central banks will be a key driver for banks’ funding plans. Another driver are issuance needs of instruments for meeting the minimum requirement for own funds and eligible liabilities (MREL). In developing and exercising their funding strategies banks should also be aware of the resurgence of market volatility and a potential upcoming interest rate increase.

Operational risks in EU banks have again been on the rise. ICT-related risks are currently one of the main challenges for EU banks, with cyber risks and data security being the main drivers. At the same time, conduct and legal risks, including breach of anti-money laundering regulations, have been on the rise in 2018.

Looking forward, risks to the global economy are increasing with growing geopolitical tensions, coupled with uncertainties surrounding financial and economic conditions in emerging markets economies. Banks need to be prepared for adverse scenarios, which might impact funding, asset quality and profitability.