Abstract: A key element of the Basel III reforms are stricter capital requirements, which have been implemented with varying degrees of stringency across jurisdictions. We examine the impact of these requirements on bank profitability in the US and Europe between 2019 and 2024. We find no evidence that higher capital ratios or requirements negatively affect profitability. However, our results indicate that international differences in capital requirements can influence the profitability of banks that operate globally: Since capital requirements in a jurisdiction apply only to domestic banks and foreign subsidiaries, foreign banks operating through cross-border or branch-based activities may gain a competitive advantage. Nevertheless, the effect appears to be limited to the subsample of German significant institutions (SIs). Moreover, our analysis of policy scenarios based on the estimated spillover effects suggests that lowering capital requirements is not an effective strategy for improving bank profitability and could even be detrimental if reciprocated by foreign jurisdictions.

Abstract: We study product innovation in the UK mortgage market by analysing when and how attributes outside the traditional structure of mortgage contracts become pricing relevant. To do so, we develop a stylised framework that treats mortgage products as structured bundles of attributes, focusing on the two-part tariff, comprising interest rates and fees, to infer innovation from pricing patterns. Our empirical strategy first uses transaction-level data and exploits within-product variations over time to detect when new product features affect pricing, which we apply to the case of green mortgages. Matching Energy Performance Certificates (EPCs) to UK mortgage originations, we show that EPCs become pricing-relevant in 2018, with lenders starting to offer pricing discounts for loans to buy properties with higher energy efficiency. We also use offer-level data on advertised green products to precisely estimate pricing discounts. We detect considerable green discounts, which reach up to 15 basis points in 2022. Mortgages against high EPC properties are concentrated in new buildings, suggesting relaxed credit constraints and increased housing investment, with implications for the broader economy.

Abstract: This study analyses, from both a theoretical and empirical perspective, whether issuing green bonds improves companies’ environmental performance. The theoretical part develops a model with information asymmetries between investors and issuing companies, which can choose between polluting and clean technology. The empirical analysis, based on a global sample, compares the evolution of the ESG score – an indicator of environmental commitment – between companies that issue green bonds and those that do not. The theoretical model shows that the introduction of green bonds can bridge the information gap between companies and investors, lowering financing costs for companies that adopt clean technologies. Empirical estimates indicate that issuing green bonds has a greater impact on the environmental performance of the most polluting companies. The effect is more pronounced for bonds issued specifically to finance climate risk mitigation activities.

Abstract: The paper presents two risk-based capital frameworks for systemically important European life insurers by drawing a distinction between solvency risk and systemic risk. Solvency risk arises when the value of a life insurer’s assets falls below some threshold proportion of its liabilities. To assess solvency risk we implement the Merton-Vasicek portfolio credit risk model and determine capital adequacy of life insurers that correspond to a value-at-risk measure. We measure systemic risk as the expected capital shortfall of an insurer conditional on the overall European life insurance sector being in distress. Our results show that European life insurers have been growing in systemic risk exposure since 2007 and suggest that regulatory capital requirements should account for this. We also find evidence of interconnectedness between systemically important banks and insurance companies, as measured by the transmission of volatility shocks, which increased during periods of financial stress.

Abstract: This paper evaluates whether CO2 emission levels or emission intensities are firm characteristics that drive Swiss firms’ stock returns. We show that standard characteristics such as size and the book-to-market equity ratio are more important determinants of firm-level stock returns than are CO2 levels (intensities). Brown firms (high CO2 levels or intensities) tend to be large and exhibit low book-to-market equity ratios, whereas their green counterparts are small and exhibit high book-to-market equity ratios. This explains why return differences between brown and green firms are statistically indistinguishable from zero after controlling for exposures to standard risk factors.

Abstract: In this paper, we analyze the effects of the introduction of the liquidity coverage ratio (LCR) on banks’ funding behavior. We use changes in regulatory liquidity requirements in Switzerland as a natural experiment. Using data for the period before and after the LCR was applied for all banks in Switzerland, our dataset allows us to analyze how the introduction of the LCR affects the banks’ funding structure. Our results show that the LCR had its intended effects as banks reduced their exposure to short-term funding. At the same time, we find evidence for optimization of the LCR by banks. Banks optimize their LCR by extending the maturities of liabilities slightly over 30 days, which leads to an improvement in the LCR by 10 percentage points on average. Our results imply that it makes sense to complement the 30-day LCR with longer-term liquidity requirements to reduce cliff risks.

Abstract: We explore the macroeconomic effects of climate policies promoting the green energy transition in the euro area using an extended version of the Euro Area and Global Economy (EAGLE) model. The model differentiates between brown and green energy sectors and incorporates carbon taxes and brown capital income taxes. We analyze scenarios with unilateral and globally coordinated carbon taxes, with and without revenue redistribution to green firms and financially constrained households. Carbon taxes act as negative supply shocks, raising inflation and lowering output, while subsidies to green energy firms reduce green energy prices, supporting the transition and easing recessions. Redistribution to constrained households boosts consumption but does not accelerate the green transition. Taxes on brown capital income lower both inflation and output by acting as demand shocks. Recycling revenue from this tax to subsidize green capital investment strengthens the shift to green energy and moderates economic contractions. Global coordination of carbon taxes delivers only modest additional macroeconomic effects compared with unilateral action, as substitution in energy use outweighs international spillovers. Sensitivity analyses confirm the robustness of these findings under alternative assumptions about price rigidity, substitution elasticities and monetary policy.

Abstract: This paper examines consumers’ intended adoption of a digital euro in Austria using a discrete choice experiment. We estimate a mixed logit model to quantify the role of key attributes such as privacy, offline functionality, security against financial loss, monetary incentives, and payment form factors. Our findings indicate that security and financial incentives are the strongest drivers of adoption, while respondents do not report strong preferences among the privacy options that are laid out in the experiment. We identify significant heterogeneity in adoption likelihood across socio-demographic groups. Simulations suggest that under realistic design assumptions, approximately 45% of individuals are found to have an intention to adopt a digital euro.

Abstract: New money-like products, such as tokenized money market funds (MMFs), money market exchange-traded funds (MMETFs), and stablecoins, could be transformative for finance. These products may offer significant benefits, but like other money-like assets, they also have certain vulnerabilities. We introduce a framework to analyze the vulnerabilities of new products by comparing their features to those that contribute to vulnerabilities in MMFs. Specifically, we examine the extent to which each product engages in liquidity transformation, is subject to threshold effects, serves as a money-like asset, poses contagion risks, and has reactive investors. Our framework is useful for assessing the potential effects of novel cash-like products on the overall resilience of the financial system and how such an assessment may change as these products’ uses evolve.

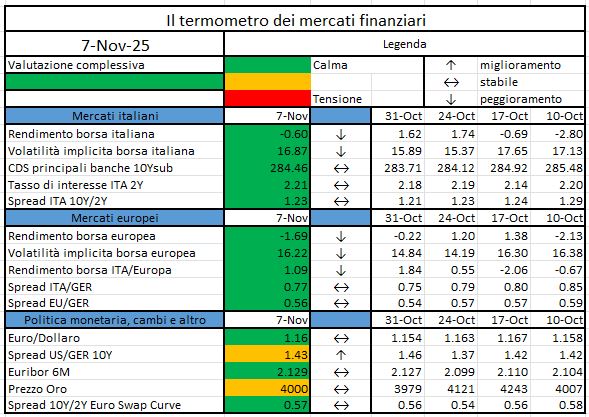

L’iniziativa di Finriskalert.it “Il termometro dei mercati finanziari” vuole presentare un indicatore settimanale sul grado di turbolenza/tensione dei mercati finanziari, con particolare attenzione all’Italia.

Rendimento borsa italiana: rendimento settimanale dell’indice della borsa italiana FTSEMIB;

Volatilità implicita borsa italiana: volatilità implicita calcolata considerando le opzioni at-the-money sul FTSEMIB a 3 mesi;

Future borsa italiana: valore del future sul FTSEMIB;

CDS principali banche 10Ysub: CDS medio delle obbligazioni subordinate a 10 anni delle principali banche italiane (Unicredit, Intesa San Paolo, MPS, Banco BPM);

Tasso di interesse ITA 2Y: tasso di interesse costruito sulla curva dei BTP con scadenza a due anni;

Spread ITA 10Y/2Y : differenza del tasso di interesse dei BTP a 10 anni e a 2 anni;

Rendimento borsa europea: rendimento settimanale dell’indice delle borse europee Eurostoxx;

Volatilità implicita borsa europea: volatilità implicita calcolata sulle opzioni at-the-money sull’indice Eurostoxx a scadenza 3 mesi;

Rendimento borsa ITA/Europa: differenza tra il rendimento settimanale della borsa italiana e quello delle borse europee, calcolato sugli indici FTSEMIB e Eurostoxx;

Spread ITA/GER: differenza tra i tassi di interesse italiani e tedeschi a 10 anni;

Spread EU/GER: differenza media tra i tassi di interesse dei principali paesi europei (Francia, Belgio, Spagna, Italia, Olanda) e quelli tedeschi a 10 anni;

Euro/dollaro: tasso di cambio euro/dollaro;

Spread US/GER 10Y: spread tra i tassi di interesse degli Stati Uniti e quelli tedeschi con scadenza 10 anni;

Prezzo Oro: quotazione dell’oro (in USD)

Euribor 6M: tasso euribor a 6 mesi.

Spread 10Y/2Y Euro Swap Curve: differenza del tasso della curva EURO ZONE IRS 3M a 10Y e 2Y;

I colori sono assegnati in un’ottica VaR: se il valore riportato è superiore (inferiore) al quantile al 15%, il colore utilizzato è l’arancione. Se il valore riportato è superiore (inferiore) al quantile al 5% il colore utilizzato è il rosso. La banda (verso l’alto o verso il basso) viene selezionata, a seconda dell’indicatore, nella direzione dell’instabilità del mercato. I quantili vengono ricostruiti prendendo la serie storica di un anno di osservazioni: ad esempio, un valore in una casella rossa significa che appartiene al 5% dei valori meno positivi riscontrati nell’ultimo anno. Per le prime tre voci della sezione “Politica Monetaria”, le bande per definire il colore sono simmetriche (valori in positivo e in negativo). I dati riportati provengono dal database Thomson Reuters. Infine, la tendenza mostra la dinamica in atto e viene rappresentata dalle frecce: ↑,↓, ↔ indicano rispettivamente miglioramento, peggioramento, stabilità rispetto alla rilevazione precedente.

Questo sito utilizza cookie tecnici e di profilazione, propri e di terze parti, per garantire la corretta navigazione, analizzare il traffico e misurare l'efficacia delle attività di comunicazione.

Questo sito Web utilizza i cookie per migliorarne l'esperienza di navigazione. I cookie classificati come necessari, sono essenziali alle funzioni di base sito e vengono sempre memorizzati nel tuo browser. I cookie di terze parti, che ci aiutano ad analizzare e capire come utilizzi questo sito, vengono memorizzati nel tuo browser solo con il tuo consenso. Di seguito hai la possibilità di disattivare questi cookie. Tieni in conto che la disattivazione di alcuni di questi cookie potrebbe influire sulla tua esperienza di navigazione.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Durata

Descrizione

cookielawinfo-checkbox-analytics

1 year

Cookie tecnico impostato dal plugin GDPR Cookie Consent che viene utilizzato per registrare il consenso dell'utente per i cookie nella categoria "Analitici".

cookielawinfo-checkbox-necessary

1 year

Cookie tecnico impostato dal plugin GDPR Cookie Consent che viene utilizzato per registrare il consenso dell'utente ai cookie.

CookieLawInfoConsent

1 year

Cookie tecnico impostato dal plugin GDPR Cookie Consent per salvare le scelte si/no dell'utente per ciascuna categoria.

viewed_cookie_policy

1 year

Cookie tecnico impostato dal plugin GDPR Cookie Consent che registra lo stato del pulsante predefinito della categoria corrispondente.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Cookie

Durata

Descrizione

_pk_id.gV3j99y0AE.0928

1 year 27 days

Cookie analitico impostato da Matomo e utilizzato per memorizzare alcuni dettagli sull'utente come l'ID univoco del visitatore

_pk_ses.gV3j99y0AE.0928

30 minutes

Cookie analitico impostato da Matomo di breve durata e utilizzato per memorizzare temporaneamente i dati della visita