POSTPONED TO JUNE 10-11, 2021 DUE TO THE COVID-19 EMERGENCY

www.mate.polimi.it/fintech

Big Data and Machine Learning are driving

a significant transformation in the financial industry. Amazing examples

include: robo-advisory; predicting frauds in payment systems; development of sophisticated

algorithmic trading strategies; systemic risk assessment; rating of

companies/financial products using a huge amount of information; development of

chatbots for customers; nowcasting of financial time series; digital marketing;

instant pricing of insurance products.

The transformation concerns the

academia and the financial industry. The goal of the conference is to bring

together academicians with different backgrounds (economists, finance experts,

data scientists, econometricians) and representatives of the financial industry

(banks, asset management, insurance companies) working in this field.

Papers on all areas dealing with Machine

Learning and Big Data in finance (including Natural Language Processing and

Artificial Intelligence techniques) are welcomed. The conference targets papers

with different angles (methodological and applications to finance).

Invited speakers:

Tomaso Aste (University College London)

Emanuele Borgonovo (Università Bocconi)

Orlando Machado (Aviva Quantum)

Juri

Marcucci (Bank of Italy)

Georgios

Sermpinis (Adam Smith Business School, University of Glasgow)

Submission of the papers deadline: March 30th, 2021

Notification deadline: April 20th, 2021

Scientific

Committee:

Emilio Barucci (Politecnico di Milano, chair), Filippo Della Casa (UNIPOL), Paolo

Giudici (Università di Pavia), Daniele Marazzina (Politecnico di Milano), Andrea

Prampolini (Banca IMI), Marcello Restelli (Politecnico di Milano).

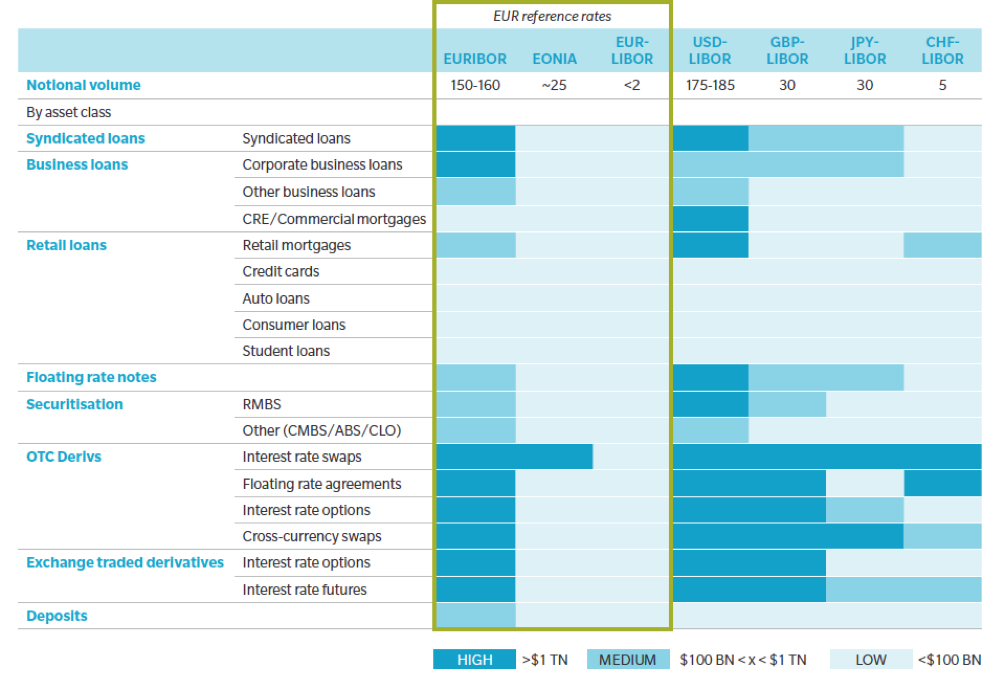

I tassi IBOR svolgono un ruolo fondamentale nei mercati

finanziari: in particolare il LIBOR è il tasso di interesse predominante per i

contratti (ad esempio interest rate swap, mutui, obbligazioni a tasso

variabile) nelle valute USD, GBP, CHF e JPY, mentre l’EURIBOR è il tasso più

diffuso per i contratti dell’area Euro (cfr. Figure 1).

A seguito della crisi finanziaria, tuttavia, la loro affidabilità e coerenza sono state messe in discussione per le acclarate manipolazioni e per il calo della liquidità del mercato interbancario. La crisi ha inoltre determinato una esplosione delle basi quotate fra tassi che differiscono per divisa o tenor, con conseguente moltiplicazione delle curve di tasso necessarie per valutare a mercato gli strumenti finanziari, e la necessità di gestire il corrispondente basis risk [1]. Tali basi sono la conseguenza del meccanismo di fixing dei tassi, riferiti a depositi interbancari a termine unsecured, e riflettono essenzialmente il rischio di credito e liquidità delle banche partecipanti (IBOR panel banks).

A partire dal 2009, le autorità e gli operatori del mercato hanno

intrapreso una serie di iniziative per rinnovare la governance dei principali

tassi d’interesse di riferimento e per individuare nuovi tassi basati su

transazioni reali in mercati di riferimento stabili e liquidi. In particolare,

i “Principles for Financial Benchmarks” emanati da IOSCO nel 2013 stabiliscono

4 aspetti principali per la determinazione dei tassi benchmark: Governance,

Quality of Benchmark, Quality of Methodology ed Accountability. Tali principi

sono stati accolti nell’area Euro dalla Benchmark Regulation (BMR), che

dichiara i tassi EURIBOR ed EONIA come “critical benchmark” ed impone quindi,

entro due anni dall’entrata in vigore (ovvero entro il 1 gennaio 2020), una

loro revisione per renderli aderenti oppure una loro sostituzione.

Il Financial Stability Board (FSB) ha raccomandato di rafforzare

tali tassi di interesse, ancorandoli a transazioni osservabili, consigliando lo

sviluppo di nuovi tassi risk free (RFR). A questo fine sono stati predisposti

cinque Working Group per le principali valute, che hanno individuato i

rispettivi RFR alternativi: in tutti i casi si tratta di tassi overnight

(secured per alcune divise ovvero unsecured per altre). Per la divisa USD è

stato scelto il tasso SOFR (Secured Overnight Financing Rate), mentre per EUR è

praticamente definito il nuovo tasso ESTER (Euro Short Term Rate, unsecured). I

tassi overnight, specialmente secured, non sono strettamente tassi privi di

rischio, ma possono essere considerati come buone approssimazioni in tal senso.

Nel luglio 2018 AFME, ICMA, ISDA, SIFMA e SIFMA AMG hanno

pubblicato l’esito della consultazione rivolta agli operatori di mercato, nella

quale vengono identificati i punti di attenzione della riforma dell’IBOR e le

raccomandazioni sugli step da effettuare per prepararsi al passaggio ai nuovi

RFR e dalla quale è emerso che esistono carenze sostanziali circa la

consapevolezza della tematica e gli step finora intrapresi per gestire la

transizione.

Transizione

I nuovi contratti conclusi dopo la scadenza BMR (1° gennaio 2020)

dovranno essere riferiti ai nuovi RFR. I contratti pre-esistenti (legacy

contracts) potranno essere re-indicizzati ai nuovi RFR oppure, se continueranno

ad essere pubblicati, contare ancora sui vecchi tassi IBOR. In entrambi i casi

sarà necessaria una modalità di transizione (“fallback”) verso i nuovi RFR.

Un passaggio molto importante in tale transizione sarà la

costruzione di una struttura a termine per i tassi RFR, sostitutiva

dell’analoga struttura a termine oggi quotata per i tassi IBOR sotto forma di

tassi di deposito, Futures, FRA (Forward Rate Agreement), e Swap. I nuovi RFR,

non disponendo di una struttura a termine con diverse scadenze, richiedono la

definizione di una regola per costruire dei tassi a termine. Ad esempio il

tasso a 3 mesi può essere costruito come composizione semplice dei tassi overnight

sul periodo. Questo tipo di indicizzazione è già ad oggi utilizzata per gli

strumenti di tipo OIS (Overnight Indexed Swap) scambiati sul mercato OTC. Sarà

poi necessario lo sviluppo di un mercato OTC liquido per tali strumenti

finanziari.

L’ISDA ha avviato un’iniziativa a livello internazionale per

identificare regole di fallback condivise per gli strumenti derivati, le quali

entreranno in vigore nel momento dell’interruzione permanente nella

contribuzione degli attuali benchmark. La soluzione di fallback si basa

sull’individuazione di un term adjustment e di uno spread adjustment da

applicare al RFR individuato. A luglio 2018, l’ISDA ha lanciato una prima

consultazione con la proposta di 4 metodologie alternative per il calcolo del

term adjustment e 3 metodologie per il calcolo dello spread adjustment, per le

divise GBP, CHF, JPY, i cui risultati sono attesi entro dicembre 2018. Una

successiva consultazione verrà lanciata per USD ed EUR nel 2019.

Tale metodologia, una volta definita e condivisa, sarà tuttavia applicabile per i soli derivati stipulati sotto ISDA agreement, mentre per gli altri strumenti (e.g. derivati non-ISDA, mutui, titoli) la conversione dovrà essere stabilita e non necessariamente avrà luogo con metodi analoghi, con il rischio di far emergere possibili basis mismatch e conseguenti conflitti contrattuali.

Area Euro

La normativa BMR ha sancito la fine dei tassi EONIA ed EURIBOR

così come li conosciamo. L’European Money Markets Institute (EMMI),

amministratore di entrambi i tassi, sta effettuando una revisione delle

metodologie attuali.

Per quanto riguarda l’EONIA, dopo una fase di studio, l’EMMI ha

ritenuto che la liquidità di mercato alla base del meccanismo di formazione

dell’EONIA non sia sufficiente per renderlo conforme alla BMR, e si è resa

quindi necessaria l’identificazione di un nuovo RFR in sua sostituzione. A tal

proposito l’European Central Bank (ECB) ha instituito il Working Group

sull’Euro Risk Free Rate, che il 13 settembre 2018 ha suggerito l’ESTER

(European Short Term Rate) quale nuovo RFR per l’Euro. Mentre l’EONIA è un

tasso di lending basato su depositi interbancari overnight effettuati sulla

piattaforma Real Time Gross Settlement (RTGS) operata dall’ECB, ESTER è un

tasso borrowing basato delle transazioni riportate dalle banche tramite il

Money Market Statistical Reporting (MMSR), e viene calcolato come media

ponderata sui volumi superiori al milione di euro, escludendo il primo 25% e

l’ultimo 25% della distribuzione dei tassi. L’ESTER, sviluppato dall’ECB

stessa, sarà ufficialmente pubblicato a partire da ottobre 2019; nel frattempo,

viene pubblicato un tasso pre-ESTER (osservazioni giornaliere a partire dal

marzo 2017 con la medesima metodologia di calcolo utilizzata a tendere) allo

scopo di familiarizzare con il nuovo tasso. I dati finora pubblicati dimostrano

che pre-ESTER è inferiore all’EONIA di circa 8-9 bps e maggiormente stabile

(minore volatilità storica e minori spike).

Per quanto riguarda l’EURIBOR, EMMI ha definito una metodologia

ibrida, attualmente in consultazione, che mira a superare le problematiche

dell’attuale metodologia di calcolo con lo scopo di ottenere un tasso che

minimizzi le possibilità di manipolazione e risulti ancorato a transazioni

osservabili e resistente agli stress del mercato. Nel caso in cui tale

metodologia venisse accettata dai regolatori come aderente ai principi IOSCO e

la BMR (scadenza 1° gennaio 2020), il nuovo EURIBOR potrebbe presumibilmente

essere il naturale successore dell’EURIBOR attuale. Nel caso in cui, invece,

l’EURIBOR subisse la medesima sorte del LIBOR, anche l’area Euro si troverà ad

affrontare le medesime problematiche delle altre principali divise. Al

riguardo, nello stesso documento in cui veniva sancita la scelta dell’ESTER

come nuova tasso risk free, il Working Group sull’Euro RFR ha suggerito di

utilizzare l’ESTER come base di partenza per costruire un nuovo tasso benchmark

in sostituzione dell’EURIBOR.

Impatti

A seguito della riforma, che avrà un impatto trasversale a tutti i

mercati, le aree in cui si possono individuate gli effetti più importanti

riguardano la liquidità degli strumenti di mercato indicizzati ai nuovi tassi,

la costruzione di nuove curve di tasso e superfici di volatilità, la modifica

delle metodologie di pricing, delle coperture, e il calcolo dei rischi. Saranno

inoltre di primaria importanza gli aspetti legali, con una possibile revisione

di tutti i contratti indicizzati ai tassi oggetto di transizione, e la gestione

della clientela per gestire possibili effetti di mismatching e di litigation.

Inoltre, si porrà la necessità di effettuare modifiche ai processi aziendali ed

alle infrastrutture IT. Al riguardo, sarà necessario porre molta attenzione

sulla governance complessiva del processo di transizione, al fine di assicurare

la coerenza tra gli impatti dei cambiamenti imposti dalla riforma e di gestire

i relativi rischi.

In particolare, per quanto riguarda i rischi di mercato, si posso

identificare i seguenti temi più rilevanti.

Contribuzioni tassi benchmark: le banche coinvolte nella contribuzione dei tassi benchmark dovranno gestire la transizione verso la contribuzione dei nuovi tassi secondo le nuove regole stabilite dagli organismi di riferimento (ECB per ESTER e prevedibilmente EMMI per EURIBOR per l’area Euro).

Dati di mercato: andrà gestita la transizione verso i nuovi tassi benchmark utilizzati come fixing per la valutazione dei contratti ed i relativi strumenti di mercato indicizzati a tali tassi. Andranno inoltre gestite le corrispondenti serie storiche per finalità di risk management (cfr. oltre).

Curve e volatilità tasso: utilizzando i nuovi strumenti di mercato indicizzati ai nuovi tassi benchmark, andranno inoltre costruite le curve di tasso e superfici di volatilità, gestendo i probabili problemi di liquidità nel caso in cui il mercato dei nuovi derivati indicizzati a RFR non sia abbastanza liquido e/o i dati non presentino una appropriata granularità. Inoltre è prevedibile un periodo di transizione in cui sarà necessario mantenere sia le vecchie curve e volatilità IBOR-based che le nuove curve e volatilità basate sui nuovi RFR.

Collateral management: in caso di revisione dei tassi di interesse utilizzati per la remunerazione del collaterale, andrà gestita la transizione verso i nuovi tassi di marginazione con conseguente revisione di tutti gli accordi di collateralizzazione.

Metodologie di pricing: le revisioni di dati di mercato, curve e volatilità tasso ed accordi di collaterale porterà probabilmente ad una conseguente revisione delle metodologie di pricing degli strumenti finanziari, che si articolano sotto vari aspetti come segue.

La revisione dei tassi di remunerazione del collaterale implicherà un adeguamento delle curve di scontro utilizzate per l’attualizzazione dei flussi futuri, con conseguenti impatti di sensitivity e P&L.

Un ulteriore impatto può determinarsi negli aggiustamenti valutativi, in particolare nelle misure di credit/debt/funding value adjustment (CVA/DVA/FVA) relative alle operazioni non soggette a collateralizzazione, dovuto all’impatto sulle esposizioni future e allo spread di finanziamento.

Possibili fasi di illiquidità e di passaggio di curve e volatilità tasso potranno determinare problemi di calibrazione dei modelli di pricing e conseguenti instabilità di prezzi, sensitivity e P&L.

In caso di dismissione dei tassi IBOR in favore di tassi risk free si avrà una semplificazione nel numero delle curve e volatilità di tasso necessarie per valutare gli strumenti, ed una semplificazione delle corrispondenti sensitivity (delta e vega in particolare). Di conseguenza si potrà determinare anche una semplificazione dei modelli di pricing, con un ritorno di fatto al mondo mono-curva risalente al periodo pre-crisi 2007.

Scenari storici: le nuove curve e volatilità tasso potrebbero non avere, dapprincipio, sufficiente profondità storica per costruire degli scenari storici, con conseguente impatto sulle metriche di rischio che si basano sui dati di mercato storici (e.g. historical VaR).

Trading vs Banking Book: date le diverse composizioni e metriche di rischio, si avranno impatti diversi: in particolare, per il Trading Book si rileverà un impatto su VaR, sensitivity, CCR e CVA, mentre per il Banking Book la transizione avrà effetti sulle masse di Bond, Loan e altri strumenti di cartolarizzazione, sia in termini di liquidità che in termini di rischio di tasso di interesse.

Basis risk: nel caso in cui l’adozione dei nuovi RFR avvenga a velocità diverse, ad es. più velocemente per i derivati e più lentamente per gli strumenti cash, anche in funzione della divisa, sarà necessario gestire una situazione ibrida con diverse asset class esposte a diversi tassi ed il conseguente rischio base.

Impatti sul capitale: la transizione verso i nuovi tassi benchmark richiederà l’identificazione dei possibili impatti sulle metriche di assorbimento di capitale; ad esempio, la mancanza di dati storici sui nuovi RFR potrebbe avere degli impatti alla luce della nuova regolamentazione per il Trading Book (FRTB), dove un punto cruciale per il calcolo delle metriche è la distinzione fra “modellable” e “non-modellable risk factors”.

Modelli Interni di Rischio: le eventuali variazioni di modello andranno gestite nell’ambito delle regole vigenti per i modelli interni (cfr. EBA RTS 2016/07 e manuale TRIM).

Figure 1: Notional outstanding balances by reference rate, order of magnitude US$ Trillion as of Dec 2017. Source: Oliver Wyman, Jun.2018

Note

[1] Ad esempio, per gestire i derivati di tasso in divisa EUR il mercato utilizza 5 curve (OIS, EURIBOR 1M, 3M, 6M, 12M) e almeno 6 superfici di volatilità (Cap/Floor EURIBOR 1M, 3M, 6M, 12M, Swaption EURIBOR 3M, 6M). Molte altre curve sono necessarie per gestire derivati e/o collateral cross currency.

The growing relevance of sustainable finance has led investors, financial institutions and regulators to pay increasing attention to the information content of ESG variables. The article Returns under the lens: the importance of ESG factors, by Gabriele Ginestroni, Daniele Marazzina and Nico Rosamilia, addresses this issue from a quantitative perspective: can raw ESG metrics help predict the direction of future stock returns?

Unlike much of the existing literature, the study does not focus only on aggregate ESG scores, whose construction often depends on proprietary methodologies adopted by data providers. Instead, it analyses the underlying ESG metrics directly, with the aim of assessing whether these data, once properly cleaned and processed, contain useful signals for financial forecasting.

The empirical analysis considers MSCI ACWI constituents over the period 2016–2022, focusing on the manufacturing, financial and information sectors in the United States and Europe. The forecasting problem is framed as a classification task: predicting the direction of one-year-ahead stock returns using ESG metrics, financial indicators and past returns.

A key contribution of the paper is the development of an ESG-oriented data cleaning pipeline, designed to deal with the high dimensionality, missing values and strong heterogeneity that typically characterize ESG datasets across sectors and regions. Several machine learning models are then compared, including tree-based methods and gradient boosting techniques. The results show that XGBoost achieves the best predictive performance.

The study also finds that raw ESG variables provide a meaningful and complementary contribution with respect to traditional financial indicators. In particular, a SHAP-based feature importance analysis shows that Environmental and Governance factors are generally the most relevant for prediction, while Social metrics become more important in specific sectoral and geographical contexts.

Overall, the results suggest that ESG information should not be considered only from the perspective of sustainability reporting or regulatory compliance. When properly processed, raw ESG metrics may also represent useful quantitative signals for strategic asset allocation, portfolio construction and risk management. The proposed approach is especially suited to annual investment horizons and low-turnover strategies, rather than short-term tactical trading.

Abstract: Internal ratings-based models play a central role in bank risk management and regulatory capital determination, yet their validation remains methodologically challenging and operationally resource-intensive. In this paper, we contribute to the quantitative validation of probability of default models through a systematic backtesting exercise using a new proprietary dataset collected by the European Banking Authority between 2017 and 2024. We propose a generalised correction to the canonical binomial test that simultaneously accounts for both asset and serial correlation and is supported by extensive simulations. Acknowledging the iterative nature of model validation, we use order statistics to identify persistent miscalibrations over time. We present an approach to aggregate the results of backtesting procedures, which are typically designed for bank level evaluation, whereas our focus is to provide evidence on the performance of the models across EU banks. Empirically, we find that the share of miscalibrated exposures of the small and medium-sized enterprises corporates asset class ranges from around 3.0% under realistic assumptions to a conservative upper bound of 16.7% implied by the canonical binomial test. We also quantify the impact on capital requirements and show that prudent model recalibrations would reduce system-wide Tier 1 capital ratios by 4 to 10 basis points. By offering scalable backtesting tools and enhancing transparency, we support more effective supervisory oversight and contribute to restoring market confidence in internal models.

Abstract: This paper applies machine learning methods and anomaly detection to sudden stop analysis of portfolio flows. Using the isolation forest methodology, univariate as well as bivariate sudden stops of equity and bond fund flows to emerging markets are generated. An anomaly score and an anomaly classification are provided. The results point to an increase in anomalous portfolio flows to emerging markets in recent years. In addition, the isolation forest methodology appears to yield better results than the traditional approach to sudden stop analysis in classifying anomalies connected with the recent capital flow volatility related to the outbreak of the COVID-19 pandemic as well as the interest rate reversal in advanced economies in recent years. The bivariate approach to anomaly detection is better able to identify anomalous episodes of financial stress, where both equity and bond markets are simultaneously affected. Most of the classified anomalies are related to fund flow stops (i.e. simultaneous stops to both equity and bond flows) or surges (i.e. surges in both equity and bond flows). In general, univariate and bivariate anomaly detection using machine learning techniques can play an important part and lead to a better understanding of sudden stops and surges.

Abstract: We analyse the macroeconomic impact of stablecoins using a quantitative macroeconomic model. Stablecoins influence the economy through two opposing channels: (i) a bank lending channel, as household demand for stablecoins raises deposit rates, increases bank funding costs, and reduces loan supply; and (ii) a fiscal space channel, as stablecoin issuers’ demand for Treasury bills lowers sovereign borrowing costs, expands fiscal space for tax reductions or higher spending. Calibrated to the U.S., the model predicts that widespread stablecoin adoption modestly reduces long-run output, as the bank lending channel outweighs the fiscal space channel. However, the overall long-run impact may shift under alternative scenarios about stablecoin reserve asset regulation, the level of public debt and the strength of foreign demand. Moreover, the fiscal space channel activates more quickly than the bank lending channel, resulting in significantly positive short-term output effects during the transition phase. Additionally, the model suggests a strengthening of monetary policy transmission via the bank lending channel

Abstract: We propose a framework for constructing fixed-income portfolios of sovereign bonds that integrates financial and environmental considerations. Central to our approach is the introduction of carbon returns, a concept analogous to financial returns, modeled as random variables to capture the inherent uncertainty of future carbon emissions. Based on the financial and carbon return profiles of individual countries’ sovereign bonds, we employ an algorithm inspired by Hierarchical Risk Parity (HRP) to construct portfolios that balance each country’s contribution to the portfolio’s tail risk, as measured by expected shortfall, of financial and carbon returns. Focusing on developed market sovereign bonds, our results demonstrate that it is possible to design portfolios that effectively align decarbonization objectives with financial performance, both in-sample and out-of-sample, while accommodating diverse investor preferences.

Abstract: We study the optimal design of a central bank digital currency (CBDC) in an economy where private payment service providers (PSPs) collect and monetize transaction data and may have market power. Payments data create social benefits through law enforcement and monitoring but also impose privacy costs and negative externalities by enabling profiling and surplus extraction. In our model, the central bank chooses CBDC fees, transaction rewards, and data-collection intensity, taking into account their effects on private payment adoption. We show that a data-collecting CBDC can either raise or lower private payment adoption and aggregate data production relative to cash, depending on the balance between PSP market power and the social costs of privately monetized data. In a calibration to the U.S. economy, the introduction of CBDC raises aggregate data collection, private PSP market share, and PSP profits. But when PSP competition is stronger, data are more valuable, or data-processing costs are lower, the optimal CBDC policy reduces aggregate data production if negative data externalities are sufficiently strong.

Abstract: Drawing on a novel dataset of more than 10,000 speeches from 1914 to 2024, we track the evolution of Federal Reserve communication and identify three stylized facts. (1) Although the overall volume of speeches has declined over the past decade, the composition of Fed communication has remained notably consistent for forty years, with Federal Reserve Bank (FRB) presidents accounting for the majority of public engagements. Variation in communicative participation is driven primarily by dispositional factors, including professional background, gender, and other speaker-specific idiosyncrasies, rather than the particular time frame in which the speeches were delivered. (2) While governors’ communication reacts to financial stability, FRB presidents’ schedules remain decoupled from both regional shifts in their districts and broader macroindicators. (3) A “complexity paradox” has emerged: while the syntactic structure simplifies during crises, the conceptual density increases. When adjusted for abstractness, the communication patterns of governors and FRB presidents appear remarkably similar.

Abstract: This paper investigates the relationship between the optimal level minimum capital requirements aimed at preventing moral hazard by banks and banks’ incentives to invest in process innovation aimed at improving operational efficiency. We extend Hellmann et al (2000)’s dynamic model of banking competition to show that the imposition of minimum effective capital requirements aimed at preventing excessive risk-taking by banks supports, rather than hinders, investment in process innovation, thanks to the longer time horizon over which banks can expect to benefit from the efficiency improvement thereof. This is because investments in process innovation will be more valuable if banks act prudently. This in turn reduces the incentive for moral hazard with implications for the optimal level of minimum capital requirements.

Abstract: We analyse how risk-based capital requirements shape competition and credit allocation in the UK unsecured Small and Medium-sized Enterprises (SME) lending market using confidential loan-level data. Motivated by empirical patterns, we develop and estimate a structural model with screening, asymmetric information, and imperfect competition, in which banks and non-bank lenders differ in regulatory treatment. We estimate lender-specific costs and screening precision, and show how these features jointly account for the observed lender market shares across borrower risk and loan size segments. Our results indicate that regulation interacts with heterogeneity in information processing and costs to shape equilibrium pricing and credit allocation, with non-bank lending reflecting not only regulatory differences but also comparative advantages in screening technology. Our model provides a quantitative framework for evaluating regulatory policy in markets with both regulated and non-regulated intermediaries.

Abstract: Emerging economies that are large oil producers have sizable external debt, their sovereign risk rises when oil prices fall, and many of them have defaulted in the past. Interestingly, oil output reduces country risk on impact and in the long-run,but oil reserves increase it in the long-run and reduce it only marginally on impact. We propose a model of sovereign default and oil extraction and derive analytic and quantitative findings consistent with these observations. The sovereign manages oil reserves strategically to make default less painful, and hence its sustainable debt falls. Reserves rise in the run-up to a default and the co-movement of reserves and country risk in response to oil-price shocks switches from negative initially to positive afterwards. These results extend to a setup with rare, large and uncertain oil discoveries. Defaults occur with less severe drops in GDP and oil prices but after long dry spells in discoveries.

Questo sito utilizza cookie tecnici e di profilazione, propri e di terze parti, per garantire la corretta navigazione, analizzare il traffico e misurare l'efficacia delle attività di comunicazione.

Questo sito Web utilizza i cookie per migliorarne l'esperienza di navigazione. I cookie classificati come necessari, sono essenziali alle funzioni di base sito e vengono sempre memorizzati nel tuo browser. I cookie di terze parti, che ci aiutano ad analizzare e capire come utilizzi questo sito, vengono memorizzati nel tuo browser solo con il tuo consenso. Di seguito hai la possibilità di disattivare questi cookie. Tieni in conto che la disattivazione di alcuni di questi cookie potrebbe influire sulla tua esperienza di navigazione.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Durata

Descrizione

cookielawinfo-checkbox-analytics

1 year

Cookie tecnico impostato dal plugin GDPR Cookie Consent che viene utilizzato per registrare il consenso dell'utente per i cookie nella categoria "Analitici".

cookielawinfo-checkbox-necessary

1 year

Cookie tecnico impostato dal plugin GDPR Cookie Consent che viene utilizzato per registrare il consenso dell'utente ai cookie.

CookieLawInfoConsent

1 year

Cookie tecnico impostato dal plugin GDPR Cookie Consent per salvare le scelte si/no dell'utente per ciascuna categoria.

viewed_cookie_policy

1 year

Cookie tecnico impostato dal plugin GDPR Cookie Consent che registra lo stato del pulsante predefinito della categoria corrispondente.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Cookie

Durata

Descrizione

_pk_id.gV3j99y0AE.0928

1 year 27 days

Cookie analitico impostato da Matomo e utilizzato per memorizzare alcuni dettagli sull'utente come l'ID univoco del visitatore

_pk_ses.gV3j99y0AE.0928

30 minutes

Cookie analitico impostato da Matomo di breve durata e utilizzato per memorizzare temporaneamente i dati della visita