POSTPONED TO JUNE 10-11, 2021 DUE TO THE COVID-19 EMERGENCY

www.mate.polimi.it/fintech

Big Data and Machine Learning are driving

a significant transformation in the financial industry. Amazing examples

include: robo-advisory; predicting frauds in payment systems; development of sophisticated

algorithmic trading strategies; systemic risk assessment; rating of

companies/financial products using a huge amount of information; development of

chatbots for customers; nowcasting of financial time series; digital marketing;

instant pricing of insurance products.

The transformation concerns the

academia and the financial industry. The goal of the conference is to bring

together academicians with different backgrounds (economists, finance experts,

data scientists, econometricians) and representatives of the financial industry

(banks, asset management, insurance companies) working in this field.

Papers on all areas dealing with Machine

Learning and Big Data in finance (including Natural Language Processing and

Artificial Intelligence techniques) are welcomed. The conference targets papers

with different angles (methodological and applications to finance).

Invited speakers:

Tomaso Aste (University College London)

Emanuele Borgonovo (Università Bocconi)

Orlando Machado (Aviva Quantum)

Juri

Marcucci (Bank of Italy)

Georgios

Sermpinis (Adam Smith Business School, University of Glasgow)

Submission of the papers deadline: March 30th, 2021

Notification deadline: April 20th, 2021

Scientific

Committee:

Emilio Barucci (Politecnico di Milano, chair), Filippo Della Casa (UNIPOL), Paolo

Giudici (Università di Pavia), Daniele Marazzina (Politecnico di Milano), Andrea

Prampolini (Banca IMI), Marcello Restelli (Politecnico di Milano).

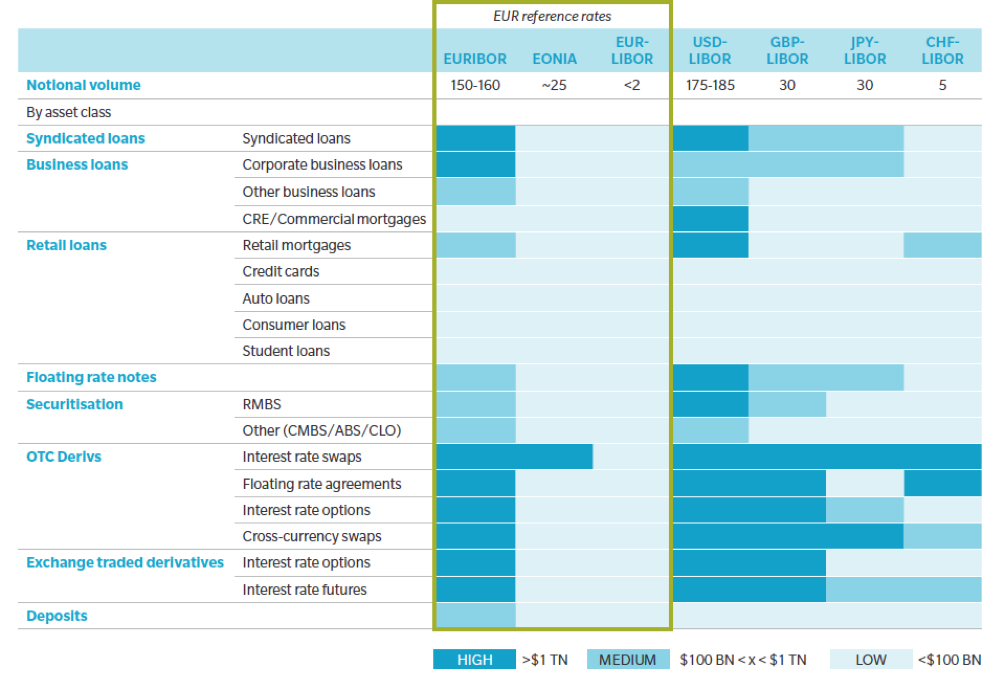

I tassi IBOR svolgono un ruolo fondamentale nei mercati

finanziari: in particolare il LIBOR è il tasso di interesse predominante per i

contratti (ad esempio interest rate swap, mutui, obbligazioni a tasso

variabile) nelle valute USD, GBP, CHF e JPY, mentre l’EURIBOR è il tasso più

diffuso per i contratti dell’area Euro (cfr. Figure 1).

A seguito della crisi finanziaria, tuttavia, la loro affidabilità e coerenza sono state messe in discussione per le acclarate manipolazioni e per il calo della liquidità del mercato interbancario. La crisi ha inoltre determinato una esplosione delle basi quotate fra tassi che differiscono per divisa o tenor, con conseguente moltiplicazione delle curve di tasso necessarie per valutare a mercato gli strumenti finanziari, e la necessità di gestire il corrispondente basis risk [1]. Tali basi sono la conseguenza del meccanismo di fixing dei tassi, riferiti a depositi interbancari a termine unsecured, e riflettono essenzialmente il rischio di credito e liquidità delle banche partecipanti (IBOR panel banks).

A partire dal 2009, le autorità e gli operatori del mercato hanno

intrapreso una serie di iniziative per rinnovare la governance dei principali

tassi d’interesse di riferimento e per individuare nuovi tassi basati su

transazioni reali in mercati di riferimento stabili e liquidi. In particolare,

i “Principles for Financial Benchmarks” emanati da IOSCO nel 2013 stabiliscono

4 aspetti principali per la determinazione dei tassi benchmark: Governance,

Quality of Benchmark, Quality of Methodology ed Accountability. Tali principi

sono stati accolti nell’area Euro dalla Benchmark Regulation (BMR), che

dichiara i tassi EURIBOR ed EONIA come “critical benchmark” ed impone quindi,

entro due anni dall’entrata in vigore (ovvero entro il 1 gennaio 2020), una

loro revisione per renderli aderenti oppure una loro sostituzione.

Il Financial Stability Board (FSB) ha raccomandato di rafforzare

tali tassi di interesse, ancorandoli a transazioni osservabili, consigliando lo

sviluppo di nuovi tassi risk free (RFR). A questo fine sono stati predisposti

cinque Working Group per le principali valute, che hanno individuato i

rispettivi RFR alternativi: in tutti i casi si tratta di tassi overnight

(secured per alcune divise ovvero unsecured per altre). Per la divisa USD è

stato scelto il tasso SOFR (Secured Overnight Financing Rate), mentre per EUR è

praticamente definito il nuovo tasso ESTER (Euro Short Term Rate, unsecured). I

tassi overnight, specialmente secured, non sono strettamente tassi privi di

rischio, ma possono essere considerati come buone approssimazioni in tal senso.

Nel luglio 2018 AFME, ICMA, ISDA, SIFMA e SIFMA AMG hanno

pubblicato l’esito della consultazione rivolta agli operatori di mercato, nella

quale vengono identificati i punti di attenzione della riforma dell’IBOR e le

raccomandazioni sugli step da effettuare per prepararsi al passaggio ai nuovi

RFR e dalla quale è emerso che esistono carenze sostanziali circa la

consapevolezza della tematica e gli step finora intrapresi per gestire la

transizione.

Transizione

I nuovi contratti conclusi dopo la scadenza BMR (1° gennaio 2020)

dovranno essere riferiti ai nuovi RFR. I contratti pre-esistenti (legacy

contracts) potranno essere re-indicizzati ai nuovi RFR oppure, se continueranno

ad essere pubblicati, contare ancora sui vecchi tassi IBOR. In entrambi i casi

sarà necessaria una modalità di transizione (“fallback”) verso i nuovi RFR.

Un passaggio molto importante in tale transizione sarà la

costruzione di una struttura a termine per i tassi RFR, sostitutiva

dell’analoga struttura a termine oggi quotata per i tassi IBOR sotto forma di

tassi di deposito, Futures, FRA (Forward Rate Agreement), e Swap. I nuovi RFR,

non disponendo di una struttura a termine con diverse scadenze, richiedono la

definizione di una regola per costruire dei tassi a termine. Ad esempio il

tasso a 3 mesi può essere costruito come composizione semplice dei tassi overnight

sul periodo. Questo tipo di indicizzazione è già ad oggi utilizzata per gli

strumenti di tipo OIS (Overnight Indexed Swap) scambiati sul mercato OTC. Sarà

poi necessario lo sviluppo di un mercato OTC liquido per tali strumenti

finanziari.

L’ISDA ha avviato un’iniziativa a livello internazionale per

identificare regole di fallback condivise per gli strumenti derivati, le quali

entreranno in vigore nel momento dell’interruzione permanente nella

contribuzione degli attuali benchmark. La soluzione di fallback si basa

sull’individuazione di un term adjustment e di uno spread adjustment da

applicare al RFR individuato. A luglio 2018, l’ISDA ha lanciato una prima

consultazione con la proposta di 4 metodologie alternative per il calcolo del

term adjustment e 3 metodologie per il calcolo dello spread adjustment, per le

divise GBP, CHF, JPY, i cui risultati sono attesi entro dicembre 2018. Una

successiva consultazione verrà lanciata per USD ed EUR nel 2019.

Tale metodologia, una volta definita e condivisa, sarà tuttavia applicabile per i soli derivati stipulati sotto ISDA agreement, mentre per gli altri strumenti (e.g. derivati non-ISDA, mutui, titoli) la conversione dovrà essere stabilita e non necessariamente avrà luogo con metodi analoghi, con il rischio di far emergere possibili basis mismatch e conseguenti conflitti contrattuali.

Area Euro

La normativa BMR ha sancito la fine dei tassi EONIA ed EURIBOR

così come li conosciamo. L’European Money Markets Institute (EMMI),

amministratore di entrambi i tassi, sta effettuando una revisione delle

metodologie attuali.

Per quanto riguarda l’EONIA, dopo una fase di studio, l’EMMI ha

ritenuto che la liquidità di mercato alla base del meccanismo di formazione

dell’EONIA non sia sufficiente per renderlo conforme alla BMR, e si è resa

quindi necessaria l’identificazione di un nuovo RFR in sua sostituzione. A tal

proposito l’European Central Bank (ECB) ha instituito il Working Group

sull’Euro Risk Free Rate, che il 13 settembre 2018 ha suggerito l’ESTER

(European Short Term Rate) quale nuovo RFR per l’Euro. Mentre l’EONIA è un

tasso di lending basato su depositi interbancari overnight effettuati sulla

piattaforma Real Time Gross Settlement (RTGS) operata dall’ECB, ESTER è un

tasso borrowing basato delle transazioni riportate dalle banche tramite il

Money Market Statistical Reporting (MMSR), e viene calcolato come media

ponderata sui volumi superiori al milione di euro, escludendo il primo 25% e

l’ultimo 25% della distribuzione dei tassi. L’ESTER, sviluppato dall’ECB

stessa, sarà ufficialmente pubblicato a partire da ottobre 2019; nel frattempo,

viene pubblicato un tasso pre-ESTER (osservazioni giornaliere a partire dal

marzo 2017 con la medesima metodologia di calcolo utilizzata a tendere) allo

scopo di familiarizzare con il nuovo tasso. I dati finora pubblicati dimostrano

che pre-ESTER è inferiore all’EONIA di circa 8-9 bps e maggiormente stabile

(minore volatilità storica e minori spike).

Per quanto riguarda l’EURIBOR, EMMI ha definito una metodologia

ibrida, attualmente in consultazione, che mira a superare le problematiche

dell’attuale metodologia di calcolo con lo scopo di ottenere un tasso che

minimizzi le possibilità di manipolazione e risulti ancorato a transazioni

osservabili e resistente agli stress del mercato. Nel caso in cui tale

metodologia venisse accettata dai regolatori come aderente ai principi IOSCO e

la BMR (scadenza 1° gennaio 2020), il nuovo EURIBOR potrebbe presumibilmente

essere il naturale successore dell’EURIBOR attuale. Nel caso in cui, invece,

l’EURIBOR subisse la medesima sorte del LIBOR, anche l’area Euro si troverà ad

affrontare le medesime problematiche delle altre principali divise. Al

riguardo, nello stesso documento in cui veniva sancita la scelta dell’ESTER

come nuova tasso risk free, il Working Group sull’Euro RFR ha suggerito di

utilizzare l’ESTER come base di partenza per costruire un nuovo tasso benchmark

in sostituzione dell’EURIBOR.

Impatti

A seguito della riforma, che avrà un impatto trasversale a tutti i

mercati, le aree in cui si possono individuate gli effetti più importanti

riguardano la liquidità degli strumenti di mercato indicizzati ai nuovi tassi,

la costruzione di nuove curve di tasso e superfici di volatilità, la modifica

delle metodologie di pricing, delle coperture, e il calcolo dei rischi. Saranno

inoltre di primaria importanza gli aspetti legali, con una possibile revisione

di tutti i contratti indicizzati ai tassi oggetto di transizione, e la gestione

della clientela per gestire possibili effetti di mismatching e di litigation.

Inoltre, si porrà la necessità di effettuare modifiche ai processi aziendali ed

alle infrastrutture IT. Al riguardo, sarà necessario porre molta attenzione

sulla governance complessiva del processo di transizione, al fine di assicurare

la coerenza tra gli impatti dei cambiamenti imposti dalla riforma e di gestire

i relativi rischi.

In particolare, per quanto riguarda i rischi di mercato, si posso

identificare i seguenti temi più rilevanti.

Contribuzioni tassi benchmark: le banche coinvolte nella contribuzione dei tassi benchmark dovranno gestire la transizione verso la contribuzione dei nuovi tassi secondo le nuove regole stabilite dagli organismi di riferimento (ECB per ESTER e prevedibilmente EMMI per EURIBOR per l’area Euro).

Dati di mercato: andrà gestita la transizione verso i nuovi tassi benchmark utilizzati come fixing per la valutazione dei contratti ed i relativi strumenti di mercato indicizzati a tali tassi. Andranno inoltre gestite le corrispondenti serie storiche per finalità di risk management (cfr. oltre).

Curve e volatilità tasso: utilizzando i nuovi strumenti di mercato indicizzati ai nuovi tassi benchmark, andranno inoltre costruite le curve di tasso e superfici di volatilità, gestendo i probabili problemi di liquidità nel caso in cui il mercato dei nuovi derivati indicizzati a RFR non sia abbastanza liquido e/o i dati non presentino una appropriata granularità. Inoltre è prevedibile un periodo di transizione in cui sarà necessario mantenere sia le vecchie curve e volatilità IBOR-based che le nuove curve e volatilità basate sui nuovi RFR.

Collateral management: in caso di revisione dei tassi di interesse utilizzati per la remunerazione del collaterale, andrà gestita la transizione verso i nuovi tassi di marginazione con conseguente revisione di tutti gli accordi di collateralizzazione.

Metodologie di pricing: le revisioni di dati di mercato, curve e volatilità tasso ed accordi di collaterale porterà probabilmente ad una conseguente revisione delle metodologie di pricing degli strumenti finanziari, che si articolano sotto vari aspetti come segue.

La revisione dei tassi di remunerazione del collaterale implicherà un adeguamento delle curve di scontro utilizzate per l’attualizzazione dei flussi futuri, con conseguenti impatti di sensitivity e P&L.

Un ulteriore impatto può determinarsi negli aggiustamenti valutativi, in particolare nelle misure di credit/debt/funding value adjustment (CVA/DVA/FVA) relative alle operazioni non soggette a collateralizzazione, dovuto all’impatto sulle esposizioni future e allo spread di finanziamento.

Possibili fasi di illiquidità e di passaggio di curve e volatilità tasso potranno determinare problemi di calibrazione dei modelli di pricing e conseguenti instabilità di prezzi, sensitivity e P&L.

In caso di dismissione dei tassi IBOR in favore di tassi risk free si avrà una semplificazione nel numero delle curve e volatilità di tasso necessarie per valutare gli strumenti, ed una semplificazione delle corrispondenti sensitivity (delta e vega in particolare). Di conseguenza si potrà determinare anche una semplificazione dei modelli di pricing, con un ritorno di fatto al mondo mono-curva risalente al periodo pre-crisi 2007.

Scenari storici: le nuove curve e volatilità tasso potrebbero non avere, dapprincipio, sufficiente profondità storica per costruire degli scenari storici, con conseguente impatto sulle metriche di rischio che si basano sui dati di mercato storici (e.g. historical VaR).

Trading vs Banking Book: date le diverse composizioni e metriche di rischio, si avranno impatti diversi: in particolare, per il Trading Book si rileverà un impatto su VaR, sensitivity, CCR e CVA, mentre per il Banking Book la transizione avrà effetti sulle masse di Bond, Loan e altri strumenti di cartolarizzazione, sia in termini di liquidità che in termini di rischio di tasso di interesse.

Basis risk: nel caso in cui l’adozione dei nuovi RFR avvenga a velocità diverse, ad es. più velocemente per i derivati e più lentamente per gli strumenti cash, anche in funzione della divisa, sarà necessario gestire una situazione ibrida con diverse asset class esposte a diversi tassi ed il conseguente rischio base.

Impatti sul capitale: la transizione verso i nuovi tassi benchmark richiederà l’identificazione dei possibili impatti sulle metriche di assorbimento di capitale; ad esempio, la mancanza di dati storici sui nuovi RFR potrebbe avere degli impatti alla luce della nuova regolamentazione per il Trading Book (FRTB), dove un punto cruciale per il calcolo delle metriche è la distinzione fra “modellable” e “non-modellable risk factors”.

Modelli Interni di Rischio: le eventuali variazioni di modello andranno gestite nell’ambito delle regole vigenti per i modelli interni (cfr. EBA RTS 2016/07 e manuale TRIM).

Figure 1: Notional outstanding balances by reference rate, order of magnitude US$ Trillion as of Dec 2017. Source: Oliver Wyman, Jun.2018

Note

[1] Ad esempio, per gestire i derivati di tasso in divisa EUR il mercato utilizza 5 curve (OIS, EURIBOR 1M, 3M, 6M, 12M) e almeno 6 superfici di volatilità (Cap/Floor EURIBOR 1M, 3M, 6M, 12M, Swaption EURIBOR 3M, 6M). Molte altre curve sono necessarie per gestire derivati e/o collateral cross currency.

Abstract: Fiat-backed stablecoins are expanding, and their issuers may attain systemic relevance as reserve portfolios grow and as they may become increasingly intertwined with financial markets. This paper analyzes the resulting risks and the design choices that can mitigate them. A detailed financial-economics discussion forms the core of the paper. It is paired with a model that captures the feedback loop between a systemic stablecoin and financial markets: redemptions deplete reserves, may prompt asset sales, depress bond market prices, thereby erode a stablecoin issuer’s solvency, and in turn trigger further redemptions. The model links design dials—capital and liquidity buffers, reserve composition, redemption gates, and others—to outcomes such as run frequency, fire sale intensity, and bond market volatility. The economics discussion and model analysis conclude that robust prudential design can substantially stabilize stablecoins and their surrounding market environment.

Abstract: We develop novel measures of stablecoin shocks and use them to identify the causal effects of stablecoin adoption on U.S. financial markets. Combining a daily narrative dataset of stablecoin-specific news with changes in the combined market capitalization of USDC and USDT, we measure high-frequency movements in stablecoin market capitalization and implement heteroskedasticity-based identification within an event-study and SVAR-IV framework. Stablecoin demand shocks have triggered persistent declines in short term Treasury yields, a depreciation of the U.S. dollar, and gradual spillovers into crypto and equity markets. We also document heterogeneous effects across firms: payment providers benefit from greater stablecoin adoption, whereas banks—including community and small banks—show no evidence of priced disintermediation risk. Our findings highlight stablecoin demand as a novel channel of asset-market transmission.

Abstract: We study competition between a welfare-maximizing public platform and a profit-maximizing private platform in a two-sided payment market. We characterize the public platform’s optimal pricing and show that it balances the benefits of increased competition against the welfare costs of network fragmentation. While introducing a public platform generally raises aggregate welfare and financial inclusion, the competing private platform may respond by raising its fees, disadvantaging merchants that continue to accept payments from the private platform. Finally, we show that cost-recovery and zero-fee mandates constrain public pricing, making welfare improvements uncertain and conditional on network effects, user switching behavior, and the degree of platform differentiation.

Abstract: Money is a coordination device underpinned by strong network effects: the more others accept a form of money, the more I wish to adopt it too. The decentralisation agenda of public permissionless blockchains undercuts these network effects and leads to fragmentation of the monetary landscape. Validators who maintain the blockchain need to be rewarded to play their role with the necessary reward increasing in the degree of dependence on other validators’ actions to sustain consensus. Since these rewards must ultimately be borne by users through congestion rents, capacity constraints are a feature, not a bug, especially for blockchains with more stringent standards for consensus. New blockchains with less stringent thresholds for consensus enter the market to serve users priced out of incumbent chains. The resulting fragmentation undercuts the very network effects that give money its social value. Stablecoins inherit this fragmentation from the blockchains on which they reside. The analysis has broader implications for the future of the monetary system.

Abstract: As central banks explore issuing digital currencies for public use, a critical design challenge is how to protect the privacy of the granular data trails digital payments leave behind. While privacy is widely recognised as a goal, policy debates often frame it as a trade-off with crime prevention—limiting ambition and reinforcing legacy design choices that assume privacy and enforcement are fundamentally incompatible. This risks replicating the data practices of commercial platforms in public infrastructure. This paper charts an alternative approach. Recent advances in privacy-enhancing technologies (PETs) now enable both strong privacy protections and verifiable compliance through programmable, rule-based auditability. By embedding such capabilities directly into system architecture, central banks can make privacy a built-in feature of digital money—strengthening institutional trust. Building on recent advances in cryptography and strategic analysis, we offer a conceptual framework that treats privacy and auditability as distinct design dimensions, and distil three design principles for privacy-protective CBDCs that remain compatible with enforcement needs. We also introduce a “PET dashboard” that maps specific technologies to CBDC system layers, highlighting where collaboration across central banks, academia, and industry is most needed.

Abstract: This paper analyses the impact of “green regulations” – i.e. those aimed at mitigating the effects of climate change and environmental externalities – on innovation, using a novel regulatory database covering the period 2008-2022 for Spain. The database identifies regulations at both the national and regional levels through textual analysis. Employing a panel data approach, we assess how different types of environmental regulations – particularly those related to renewable energy – affect firm-level innovation activities. Our findings indicate that national-level green regulations have a positive effect on innovation, whereas regional-level regulations show mixed or negligible impacts. Importantly, the interaction between national and regional regulations, measuring the simultaneous production of legal texts at both levels, can foster innovation but at a reduced pace with respect to the sole production of regulation at the national level. Given the results for regional-level regulation, our findings provide evidence in favour of the hypothesis that regulatory fragmentation due to unequal, overlapping, inconsistent or conflicting procedure across jurisdictions may diminish these benefits.

Abstract: We propose a robust semi-parametric framework for persistent time-varying extreme tail behavior, including extreme Value-at-Risk (VaR) and Expected Shortfall (ES). The framework builds on Extreme Value Theory and uses a conditional version of the Generalized Pareto Distribution (GPD) for peaks-over-threshold (POT) dynamics. Unlike earlier approaches, our model (i) has unit root-like, i.e., integrated autoregressive dynamics for the GPD tail shape, and (ii) re-scales POTs by their thresholds to obtain a more parsimonious model with only one time-varying parameter to describe the entire tail. We establish parameter regions for stationarity, ergodicity, and invertibility for the integrated time-varying parameter model and its filter, and formulate conditions for consistency and asymptotic normality of the maximum likelihood estimator. Using two cryptocurrency exchange rates, we illustrate how the simple single-parameter model is competitive in capturing the dynamics of VaR and ES, particularly in the extreme tail.

Abstract: This paper examines the role of insurance in mitigating the adverse macroeconomic effects of climate-related catastrophes. We first develop a stylised theoretical growth model which incorporates a role for natural catastrophes, climate change and insurance. This illustrates how insurance can mitigate the impact of catastrophes and articulates the potential effect of falling insurance coverage as global warming intensifies. The model also provides a basis for our empirical analysis which explores the link between insurance coverage and the macroeconomic impact of catastrophes for a sample of several thousand disaster events across 47 developed and middle income countries between 1996 and 2019. The results confirm that higher insurance coverage is associated with less severe macroeconomic consequences of disasters. With climate-related catastrophes becoming ever more frequent and severe, our findings highlight the importance of developing policies to reduce the climate insurance protection gap.

Abstract: When default losses elevate borrowing costs, expanding credit cannot stabilize the economy because default rates feed back to lending rates through bank balance sheets. Asset management companies (AMCs) break this loop by purchasing nonperforming loans at their long-run recovery values, thereby fixing the effective default rate that banks face. Government purchases of performing loans expand credit but leave this feedback intact. In a model calibrated to the eurozone, the AMC reduces quarterly default rates by 0.8 percentage points, lowers lending rates by 1.6 percentage points, and raises welfare by 0.2%. Government purchases crowd out bank deposits, contracting credit; default rates rise by 1.8 percentage points, lending rates increase by 1.2 percentage points, and welfare falls by 0.3%.

Abstract: Stock prices often react sluggishly to news, producing gradual and delayed jumps. Econometricians typically treat these sluggish reactions as microstructure effects and settle for a coarse sampling grid to guard against them. We introduce new methods to synchronize mistimed stock returns on a fine sampling grid that allow us to better approximate the true common jumps in the efficient prices of related stocks in an application to Dow 30 data. The synchronized jumps produce better jump covariance estimates and estimates of the realized jump betas with better forecasting power, and superior trading rule performance.

Questo sito utilizza cookie tecnici e di profilazione, propri e di terze parti, per garantire la corretta navigazione, analizzare il traffico e misurare l'efficacia delle attività di comunicazione.

Questo sito Web utilizza i cookie per migliorarne l'esperienza di navigazione. I cookie classificati come necessari, sono essenziali alle funzioni di base sito e vengono sempre memorizzati nel tuo browser. I cookie di terze parti, che ci aiutano ad analizzare e capire come utilizzi questo sito, vengono memorizzati nel tuo browser solo con il tuo consenso. Di seguito hai la possibilità di disattivare questi cookie. Tieni in conto che la disattivazione di alcuni di questi cookie potrebbe influire sulla tua esperienza di navigazione.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Durata

Descrizione

cookielawinfo-checkbox-analytics

1 year

Cookie tecnico impostato dal plugin GDPR Cookie Consent che viene utilizzato per registrare il consenso dell'utente per i cookie nella categoria "Analitici".

cookielawinfo-checkbox-necessary

1 year

Cookie tecnico impostato dal plugin GDPR Cookie Consent che viene utilizzato per registrare il consenso dell'utente ai cookie.

CookieLawInfoConsent

1 year

Cookie tecnico impostato dal plugin GDPR Cookie Consent per salvare le scelte si/no dell'utente per ciascuna categoria.

viewed_cookie_policy

1 year

Cookie tecnico impostato dal plugin GDPR Cookie Consent che registra lo stato del pulsante predefinito della categoria corrispondente.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Cookie

Durata

Descrizione

_pk_id.gV3j99y0AE.0928

1 year 27 days

Cookie analitico impostato da Matomo e utilizzato per memorizzare alcuni dettagli sull'utente come l'ID univoco del visitatore

_pk_ses.gV3j99y0AE.0928

30 minutes

Cookie analitico impostato da Matomo di breve durata e utilizzato per memorizzare temporaneamente i dati della visita