The European Securities and Markets Authority (ESMA), the EU’s securities regulator, today publishes two Annual Statistical Reports (Reports) analysing the European Union’s (EU) derivatives and securities markets…

Dic

17

2021

The European Securities and Markets Authority (ESMA), the EU’s securities regulator, today publishes two Annual Statistical Reports (Reports) analysing the European Union’s (EU) derivatives and securities markets…

On 15 November 2021 the Governing Council decided to increase the limit for asset purchase programme (APP) and pandemic emergency programme (PEPP) securities lending against cash collateral to €150 billion…

https://www.ecb.europa.eu//press/govcdec/otherdec/2021/html/ecb.gc211217~e4ba94a36d.en.html

Accredited investors can now invest in some of the world’s most valuable nonfungible tokens and art collections through the Bitwise Blue-Chip NFT Index Fund…

https://cointelegraph.com/news/bitwise-launches-nft-index-fund-for-accredited-investors

The “real” pit of the bear market for Bitcoin has since delivered over 2,000% gains for patient BTC hodlers…

https://cointelegraph.com/news/happy-bearday-bitcoin-it-s-been-3-years-since-btc-bottomed-at-3-1k

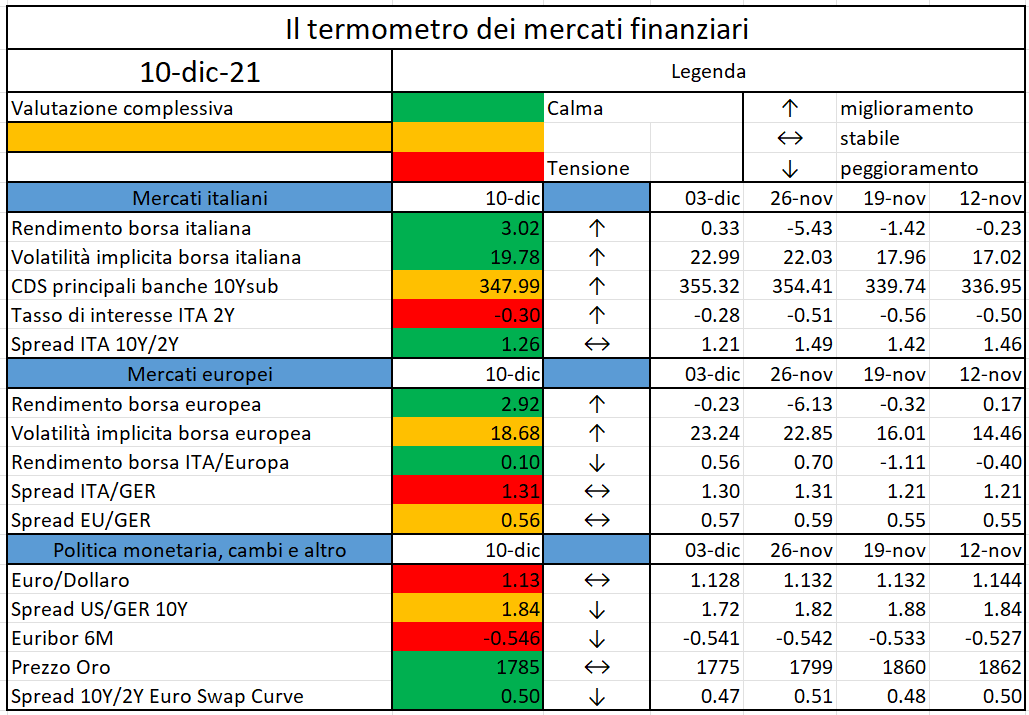

L’iniziativa di Finriskalert.it “Il termometro dei mercati finanziari” vuole presentare un indicatore settimanale sul grado di turbolenza/tensione dei mercati finanziari, con particolare attenzione all’Italia.

Significato degli indicatori

I colori sono assegnati in un’ottica VaR: se il valore riportato è superiore (inferiore) al quantile al 15%, il colore utilizzato è l’arancione. Se il valore riportato è superiore (inferiore) al quantile al 5% il colore utilizzato è il rosso. La banda (verso l’alto o verso il basso) viene selezionata, a seconda dell’indicatore, nella direzione dell’instabilità del mercato. I quantili vengono ricostruiti prendendo la serie storica di un anno di osservazioni: ad esempio, un valore in una casella rossa significa che appartiene al 5% dei valori meno positivi riscontrati nell’ultimo anno. Per le prime tre voci della sezione “Politica Monetaria”, le bande per definire il colore sono simmetriche (valori in positivo e in negativo). I dati riportati provengono dal database Thomson Reuters. Infine, la tendenza mostra la dinamica in atto e viene rappresentata dalle frecce: ↑,↓, ↔ indicano rispettivamente miglioramento, peggioramento, stabilità rispetto alla rilevazione precedente.

Disclaimer: Le informazioni contenute in questa pagina sono esclusivamente a scopo informativo e per uso personale. Le informazioni possono essere modificate da finriskalert.it in qualsiasi momento e senza preavviso. Finriskalert.it non può fornire alcuna garanzia in merito all’affidabilità, completezza, esattezza ed attualità dei dati riportati e, pertanto, non assume alcuna responsabilità per qualsiasi danno legato all’uso, proprio o improprio delle informazioni contenute in questa pagina. I contenuti presenti in questa pagina non devono in alcun modo essere intesi come consigli finanziari, economici, giuridici, fiscali o di altra natura e nessuna decisione d’investimento o qualsiasi altra decisione deve essere presa unicamente sulla base di questi dati.

The European Securities and Markets Authority (ESMA), the EU securities markets regulator, has today published the 2021 ESEF XBRL taxonomy files and an update to the ESEF Conformance Suite to facilitate implementation of the ESEF Regulation…

Today, the European Insurance and Occupational Pension Authority (EIOPA) launched a consultation on the application guidance on running climate change materiality assessment and using climate change scenarios in the Own Risk and Solvency Assessment (ORSA)…

The term metaverse has been reintroduced online due to Facebook’s announcement that they would build a VR (Virtual Reality) social network for its users…

https://www.newsbtc.com/news/company/metaverse-versus-gamefi-a-new-blockchain-war/

Gaining a deeper understanding of a popular — but widely misunderstood — concept in blockchain technology: the consensus algorithm…

Il pioniere della moderna teoria dell’Asset Allocation, primo ad aver applicato una modellistica matematica alla finanza, è stato Harry Markowitz che ha introdotto la teoria della media-varianza, stravolgendo il settore dell’Asset Management e permettendo di trovare una relazione uno a uno tra la varianza ed il rendimento di un investimento. A causa delle difficoltà nella stima dei rendimenti, la strategia di Markowitz ha mostrato spesso risultati molto distanti da quelli attesi e allocazioni di portafoglio poco diversificate.

Per superare il problema dell’instabilità della previsione dei rendimenti sono state sviluppate strategie di allocazioni di portafoglio, minimum variance – risk parity – maximum diversification, forecast free e risk-based, dipendenti solamente dai parametri di rischio degli asset in portafoglio.

La strategia Hierarchical Risk Parity è basata sulla teoria dei grafi e le tecniche di Machine Learning e ha come obiettivo la risoluzione delle inefficienze della teoria di Markowitz e delle strategie Risk Based. La strategia , costruendo una struttura gerarchica tra gli attivi rischiosi, fornisce agli investitori un approccio meno volatile e con un livello di diversificazione più elevato.

L’algoritmo di costruzione della strategia si suddivide in tre passi:

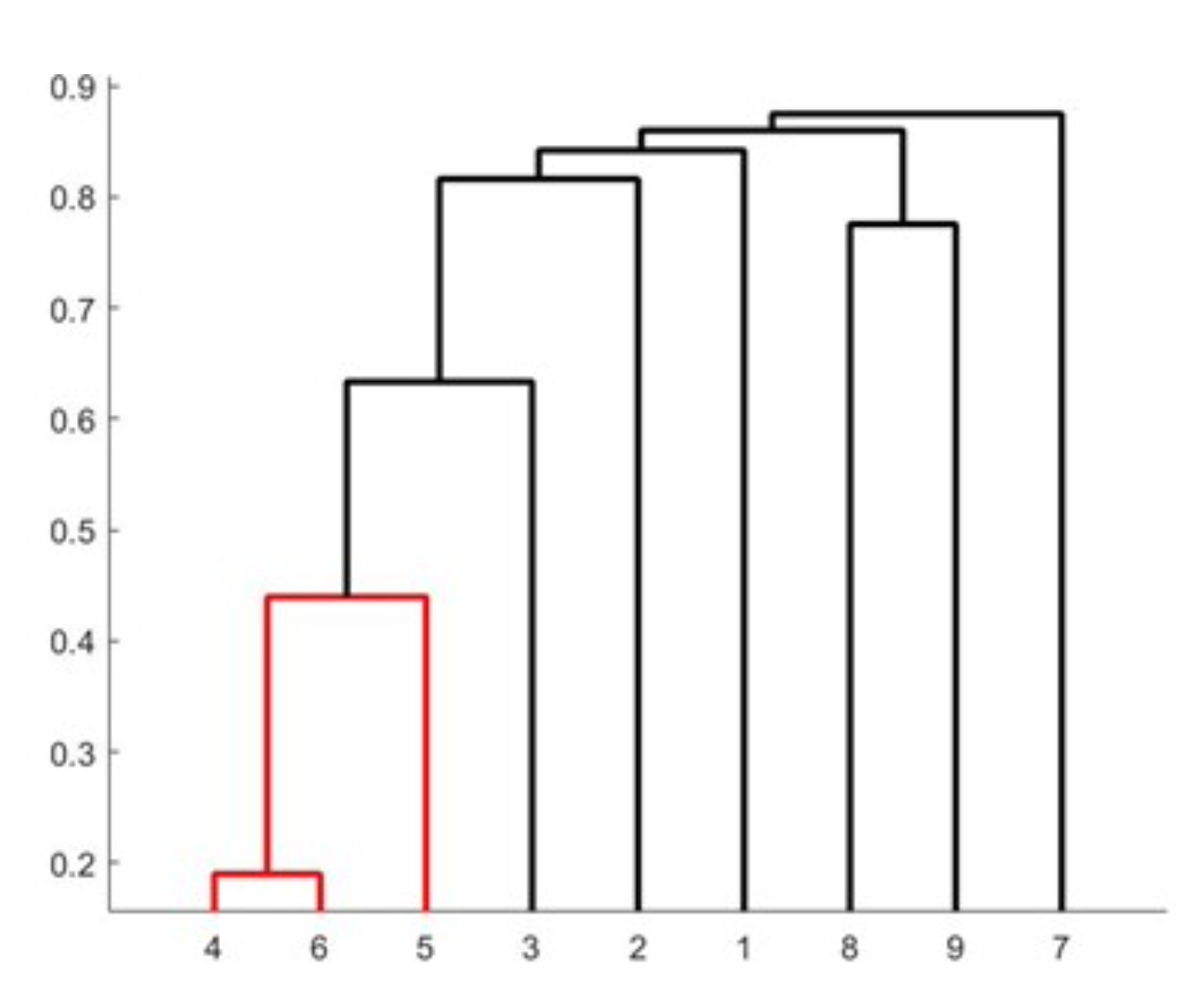

Una delle più marcate inefficienze della strategia di Markowitz è che tutti gli asset vengono considerati potenziali sostituti l’uno dell’altro senza considerare alcuna nozione gerarchica né economica. Il concetto di clusterizzazione viene introdotto per impostare un’allocazione dei pesi prima all’interno dei cluster, formati da asset che presentano una correlazione tra di loro più forte, e poi considerando il portafoglio nella sua interezza

Al termine del processo di Tree Clustering si ottiene un dendrogramma che lega gli asset maggiormente correlati mediante una struttura ad albero composta da tanti piccoli cluster come illustrato in figura 1.

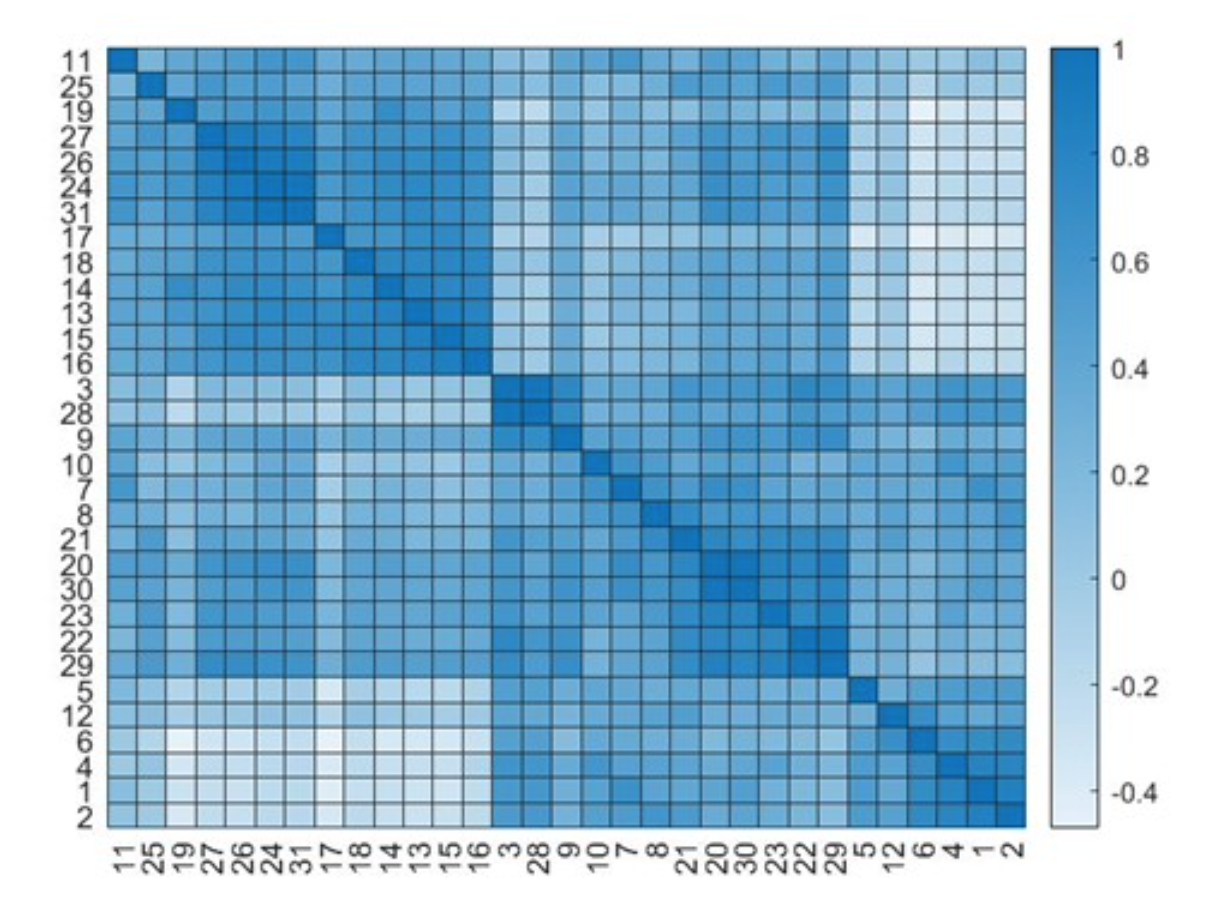

Nel processo di Quasi-Diagonalization viene costruita una matrice di correlazione riordinata secondo l’informazione ottenuta dal processo di Tree-Clustering. Il risultato è una matrice che presenta attorno alla sua diagonale gli asset maggiormente correlati tra loro, come illustrato dalla figura 2.

Recursive Bisection è l’ultimo passaggio della strategia Hierarchical Risk Parity, utile per l’assegnazione dei pesi utilizzando l’allocazione Risk Parity. L’algoritmo di recursive bisection è implementato da una funzione iterativa che assegna i pesi agli asset del portafoglio.

Per una migliore comprensione dell’efficacia della strategia HRP è molto utile un confronto tra la stessa e le strategie risk-based precedentemente nominate.

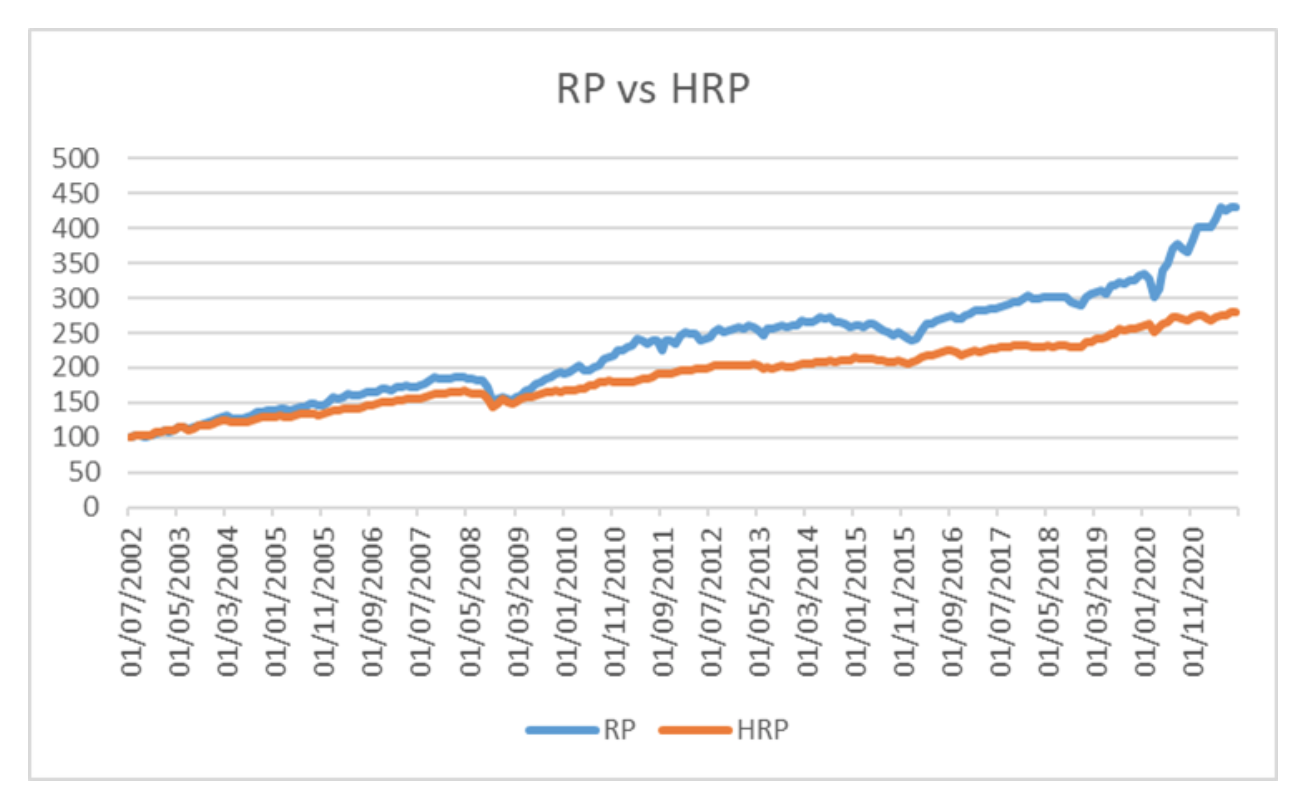

Il primo confronto proposto è basato sull’analisi storica sia della strategia Hierarchical Risk Parity che della strategia Risk Parity. Le serie storiche prese in considerazione per l’analisi ricoprono un orizzonte temporale di 24 anni, dal 2007 ad oggi. L’analisi storica, condotta su base mensile, consiste nello sviluppo di un backtesting utilizzando un in-sample-period di 60 mesi. Il risultato ottenuto dall’analisi storica, in termine di rendimento cumulato, è illustrato nella figura 3:

Dal grafico si osserva come le due curve seguono lo stesso trend nel periodo di osservazione presentando però delle differenze in termini di rendimento e volatilità:

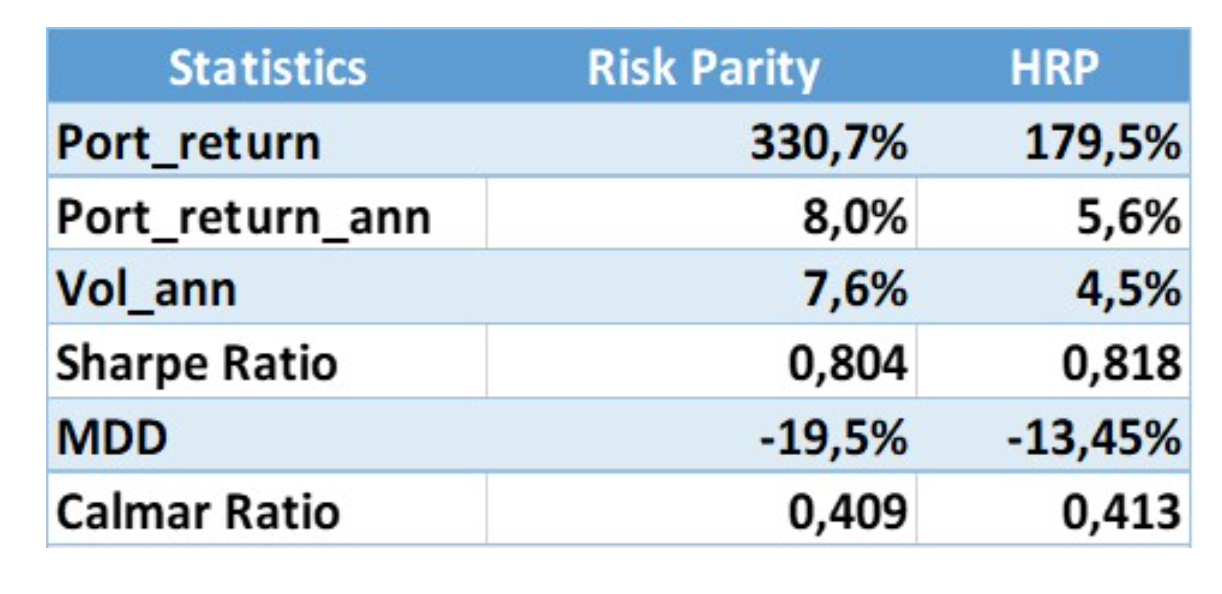

Il confronto basato sull’analisi storica prosegue mediante il calcolo delle misure di performance. Il Portfolio Return esprime il rendimento complessivo ottenuto da ogni strategia su tutto il periodo di osservazione. Per la strategia HRPil suo valore è pari a 179,5% invece per la strategia Risk Parity il Portfolio Return è 330,7%. Il calcolo della Volatility annua conferma quanto anticipato in precedenza, ossia che un rendimento maggiore paga un livello di volatilità più alto. Infatti il valore della Volatility annua per la strategia Risk Parity è del 7,6%, valore maggiore rispetto al 4,5% della Hierarchical Risk Parity. Oltre al calcolo della volatilità e del rendimento è molto utile andare a calcolare la statistica Sharpe Ratio, la quale combina l’informazione derivante dal rendimento e dalla volatilità. Con lo Sharpe Ratio, infatti, un investitore può capire effettivamente quanto il suo investimento è compensato per il rischio che lo stesso comporta. La strategia Hierarchical Risk Parity presenta uno Sharpe Ratio maggiore rispetto alla strategia Risk Parity, rispettivamente 0,818 contro 0,804, due valori comunque molto vicini tra di loro. Un’altra statistica molto utilizzata dagli asset manager per confrontare le strategie è il Maximum Drawdown che quantifica il peggior scenario possibile di perdita che il portafoglio può avere. La strategia Hierarchical Risk Parity presenta un valore del Maximum Drawdown maggiore rispetto alla Risk Parity. I valori sono rispettivamente il -13,45% ed il -19,54%. L’ultima, non per importanza, è la statistica Calmar Ratio che considera il rendimento annuo che un portafoglio ottiene aggiustato per il Maximum Drawdown. Anche in questo caso il valore migliore lo ottiene la strategia HRP: 0,413 contro 0,409 della strategia Risk Parity.

La figura 4 riassume le statistiche calcolate per le due strategie di Asset Allocation.

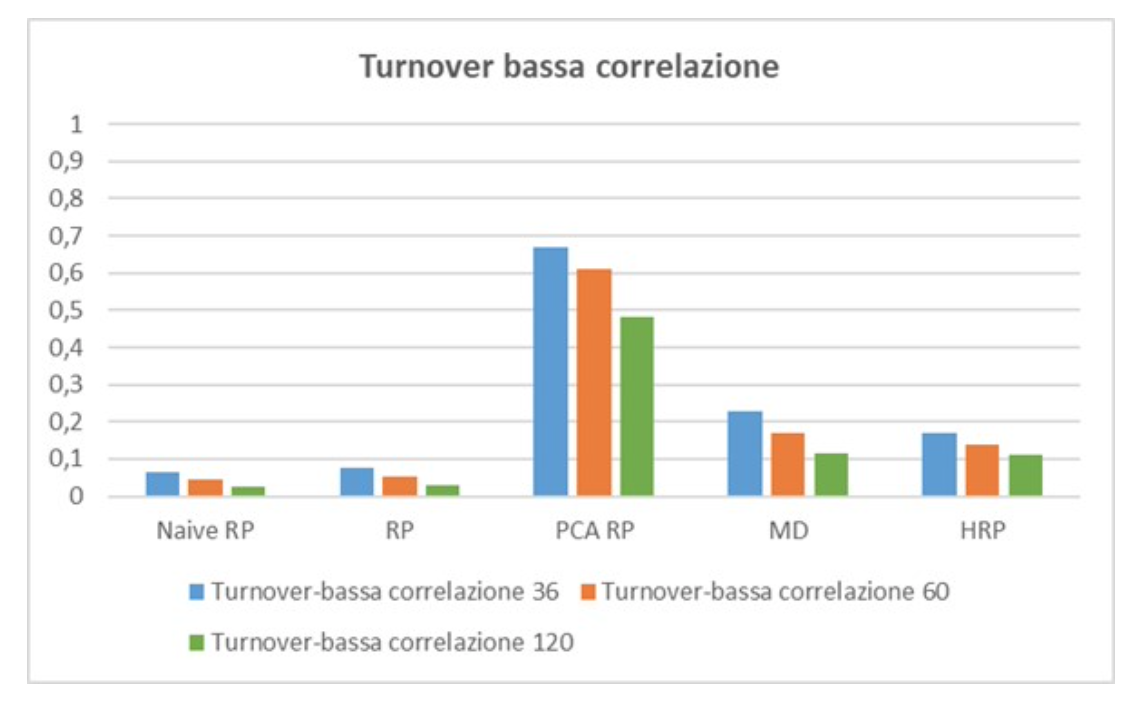

Per valutare la robustezza della strategia Hierarchical Risk Parity rispetto alle altre strategie di asset allocation è utile condurre un test di robustezza al rischio di stima della matrice di covarianza per poi confrontarne i risultati con quelli ottenuti dallo stesso test applicato alle strategie risk based, i cui valori sono tratti dal paper “A CRITICAL ASSESSMENT OF DIVERSIFICATION METRICS FOR PORTFOLIO CONSTRUCTION” di G. Pola.

Si testa la robustezza della strategia con un esperimento Montecarlo, considerando 10 asset aventi volatilità che va dall’1% al 10% e due scenari di correlazione: forte e debole. Con questi dati è possibile costruire la matrice di covarianza corretta e calcolare i pesi degli asset all’interno del portafoglio. Il passo successivo è quello di aggiungere del noise alle serie storiche per poi stimare una nuova matrice di covarianza e una nuova combinazione dei pesi degli asset all’interno del portafoglio. L’esperimento viene ripetuto per 10000 volte e si va a calcolare il turnover medio tra il portafoglio chiamato “esatto” e i 10000 portafogli simulati. L’esperimento Montecarlo si ripete su tre diversi orizzonti temporali: 36 mesi, 60 mesi e 120 mesi.

Per verificare la robustezza della strategia HRP al rischio di stima della matrice di covarianza rispetto alle altre strategie di Asset Allocation si confrontano i turnover medi di portafoglio delle strategie. Le strategie a confronto sono Maximum Diversification, Risk Parity ERC, Naive Risk Parity , PCA Risk Parity e Hierarchical Risk Parity. Dal confronto è possibile osservare come le strategie meno robuste in termini di estimation risk sono la Risk Parity PCA e il Maximum Diversification manifestando una forte dipendenza rispetto alla stima della matrice di covarianza e di conseguenza un livello di turnover maggiore rispetto alle altre strategie. Quelle più robuste invece sono la Risk Parity ERC e la Naive Risk Parity, in particolare quest’ultima dipende solamente dalla volatilità neutralizzando completamente l’effetto dei coefficienti di correlazione tra gli asset. La stategia HRP si interpone nel mezzo, presentando un Turnover leggermente più basso del Maximum Diversification e leggermente più alto della Risk Parity ERC. La figura 5 riassume quanto appena detto.

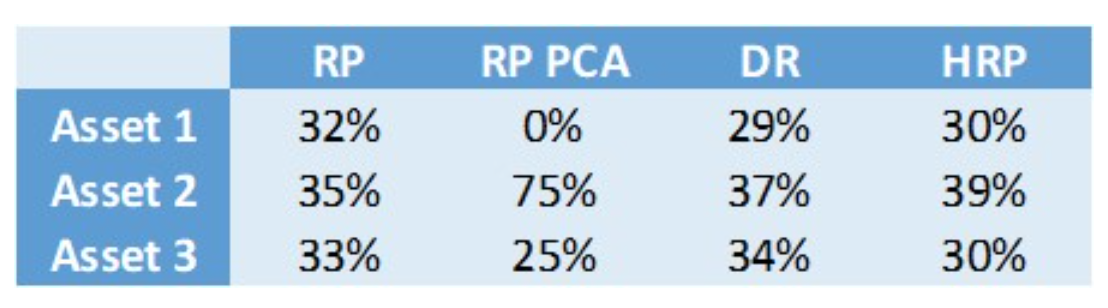

Un altro test utile al confronto tra le differenti strategie è quello della Duplication Invariance, trattato nel paper “Entropy, Diversification and the Inefficient Frontier” di G. Pola e A.Zerrad. Con il test della Duplication Invariance vengono messe a confronto le seguenti strategie: Risk Parity ERC, Risk Parity PCA, Maximum Diversification e Hierarchical Risk Parity. Se dovesse essere rispettata la Duplication Invariance allora un portafoglio, all’interno del quale un asset viene duplicato, dovrebbe produrre lo stesso risultato in termini di Asset Allocation nonostante la duplicazione dell’asset.

Nel caso di 3 asset le differenti strategie restituiscono il portafoglio in figura 6.

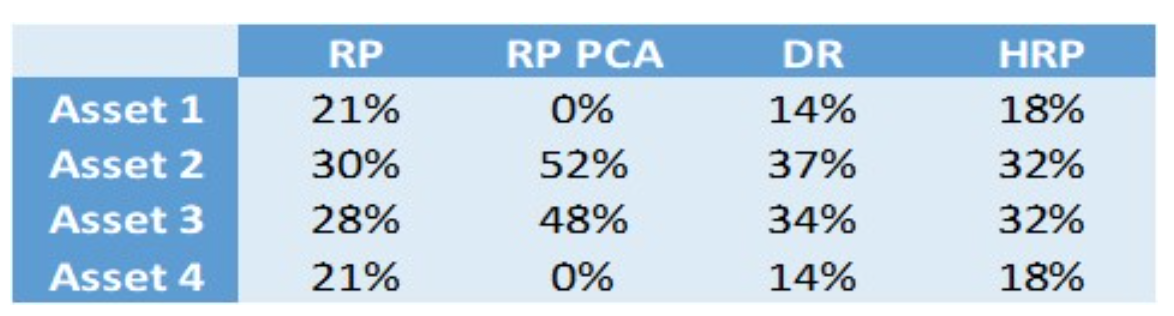

Dalla duplicazione dell’Asset 1 si ottiene invece il portafoglio in figura 7.

E’ possibile osservare come, a differenza di tutte le altre strategie analizzate, la strategia Maximum Diversification sia l’unica a rispettare il concetto di Duplication Invariance generando due portafogli identici nonostante la duplicazione dell’asset 1. Per soddisfare la duplication invariance però la strategia Maximum Diversification ha bisogno di utilizzare fortemente la correlazione tra gli asset e il prezzo da pagare è una forte sensibilità all’Estimation Risk.

In conclusione si può constatare come la strategia Hierarchical Risk Parity non presenta risultati molto distanti da tutte le strategie risk based, bensì si pone molto vicina alla Risk Parity sia in termini di robustezza nei confronti dell’estimation risk sia in termini di coerenza al concetto di Duplication Invariance. Nei confronti della tradizionale Risk Parity però la Hierarchical Risk Parity presenta delle misure di performance di portafoglio leggermente migliori trainate soprattutto da un livello di volatilità più basso. Il miglioramento in termini di Sharpe Ratio, Maximum Drawdown e Calmar Ratio infatti costano alla strategia HRP la perdita di un rendimento annuo maggiore del 2%.