The rise in long-term US interest rates has become a focus of global macro-financial concerns…

https://blogs.imf.org/2021/04/22/understanding-the-rise-in-us-long-term-rates/

The rise in long-term US interest rates has become a focus of global macro-financial concerns…

https://blogs.imf.org/2021/04/22/understanding-the-rise-in-us-long-term-rates/

Decentralized CBDCs will most likely pique the interest of the masses much more than their centralized counterparts…

https://cointelegraph.com/news/decentralization-is-the-final-frontier-for-cbdcs

Amid the COVID-19 pandemic, the role of digitalization has become central to achieving sustainability and lessening climate change…

https://cointelegraph.com/news/asia-pacific-s-solarized-digitalization-agenda-in-pandemic-times

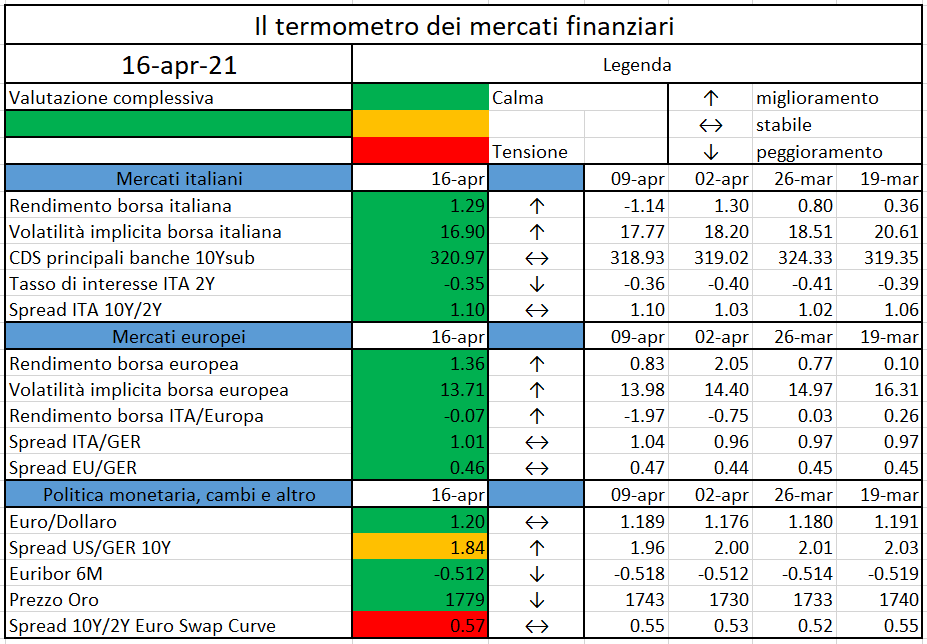

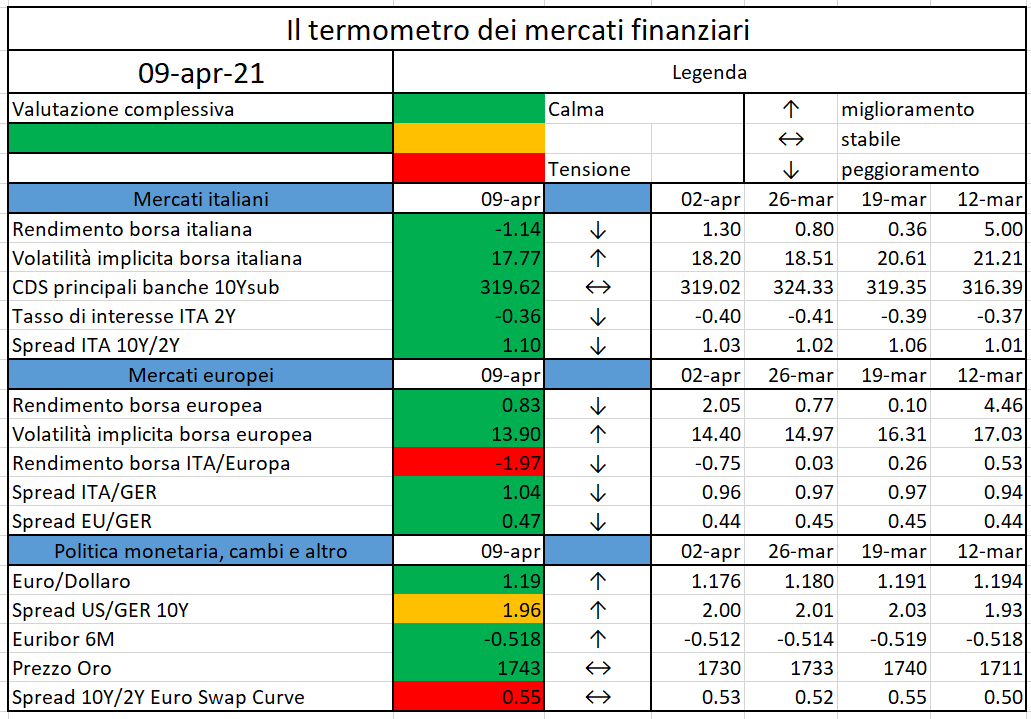

L’iniziativa di Finriskalert.it “Il termometro dei mercati finanziari” vuole presentare un indicatore settimanale sul grado di turbolenza/tensione dei mercati finanziari, con particolare attenzione all’Italia.

Significato degli indicatori

I colori sono assegnati in un’ottica VaR: se il valore riportato è superiore (inferiore) al quantile al 15%, il colore utilizzato è l’arancione. Se il valore riportato è superiore (inferiore) al quantile al 5% il colore utilizzato è il rosso. La banda (verso l’alto o verso il basso) viene selezionata, a seconda dell’indicatore, nella direzione dell’instabilità del mercato. I quantili vengono ricostruiti prendendo la serie storica di un anno di osservazioni: ad esempio, un valore in una casella rossa significa che appartiene al 5% dei valori meno positivi riscontrati nell’ultimo anno. Per le prime tre voci della sezione “Politica Monetaria”, le bande per definire il colore sono simmetriche (valori in positivo e in negativo). I dati riportati provengono dal database Thomson Reuters. Infine, la tendenza mostra la dinamica in atto e viene rappresentata dalle frecce: ↑,↓, ↔ indicano rispettivamente miglioramento, peggioramento, stabilità rispetto alla rilevazione precedente.

Disclaimer: Le informazioni contenute in questa pagina sono esclusivamente a scopo informativo e per uso personale. Le informazioni possono essere modificate da finriskalert.it in qualsiasi momento e senza preavviso. Finriskalert.it non può fornire alcuna garanzia in merito all’affidabilità, completezza, esattezza ed attualità dei dati riportati e, pertanto, non assume alcuna responsabilità per qualsiasi danno legato all’uso, proprio o improprio delle informazioni contenute in questa pagina. I contenuti presenti in questa pagina non devono in alcun modo essere intesi come consigli finanziari, economici, giuridici, fiscali o di altra natura e nessuna decisione d’investimento o qualsiasi altra decisione deve essere presa unicamente sulla base di questi dati.

Il nostro obiettivo è valutare il rendimento del nuovo BTP Futura che verrà emesso la prossima settimana dallo Stato Italiano ed è in sottoscrizione presso i risparmiatori retail.

I nuovi BTP Futura, con durata 16 anni, saranno emessi alla pari, cioè a 100 Euro, e hanno due caratteristiche principali:

I tassi cedolari definitivi saranno annunciati alla chiusura del collocamento, non potranno comunque essere inferiori ai tassi cedolari minimi garantiti appena annunciati.

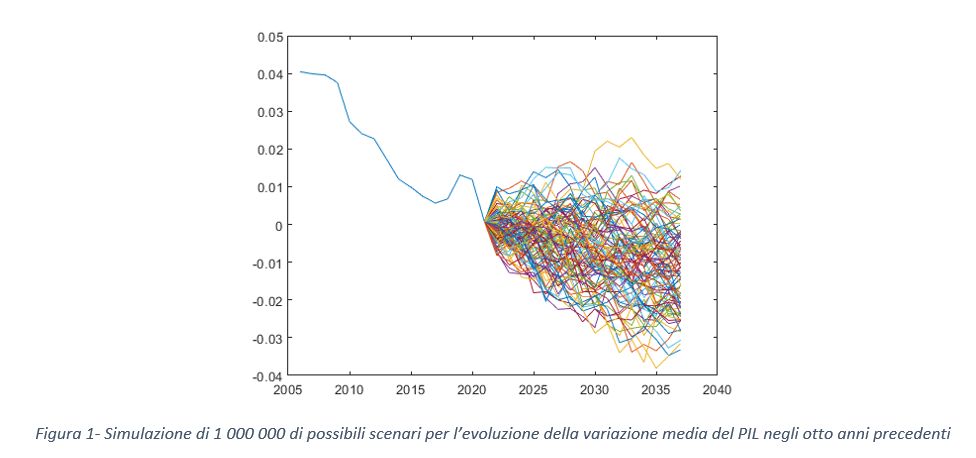

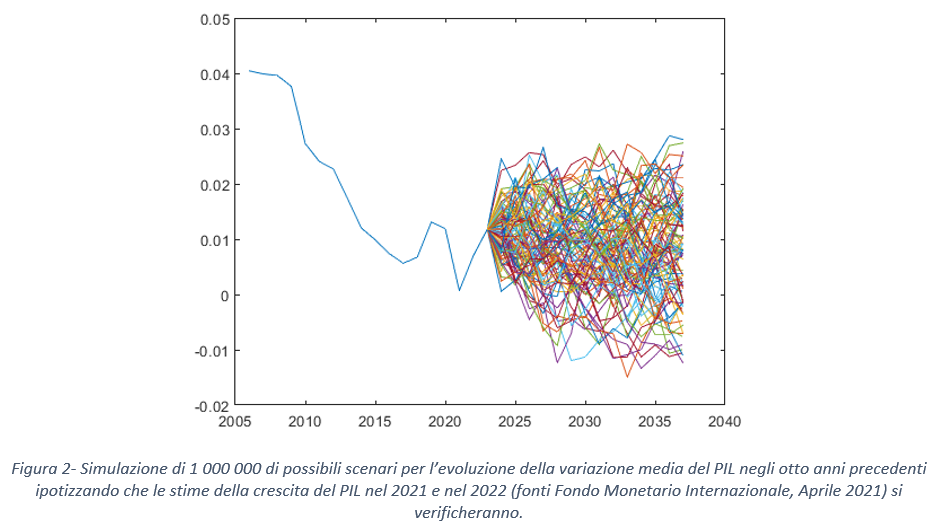

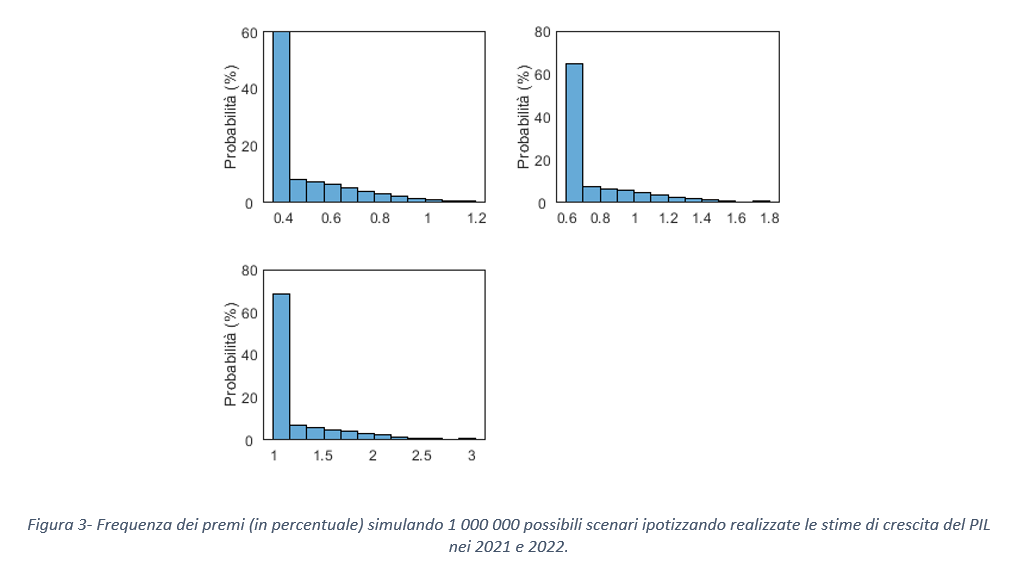

Si tratta della terza emissione dei BTP futura: della prima emissione, con un titolo decennale, avevamo parlato qui, della seconda emissione, della durata di otto anni, invece qui. Sul premio fedeltà, l’analisi svolta nei precedenti articoli, ora su un orizzonte di 16 anni, e inserendo il PIL del 2020 come nuovo dato ora disponibile, indica che la probabilità che i premi fedeltà siano superiori al valore minimo garantito è inferiore al 5%. Questa analisi, basata sulla simulazione dell’evoluzione della variazione media del PIL, Figura 1, non tiene però conto di un possibile (auspicabile) rimbalzo del PIL nel periodo post covid. Se invece ipotizziamo che le stime di crescita del PIL italiano comunicate dal Fondo Monetario Internazionale in questo mese di Aprile (+4,2% nel 2021, +3,6% nel 2022) si verificheranno, e quindi si avrà l’atteso rimbalzo dell’economia italiana – Figura 2, il nostro modello stima una probabilità del 45% che il premio fedeltà relativo ai primi 8 anni sia superiore al valore minimo, e del 39% che lo sia quello a 16 anni. La probabilità di avere il premio di fedeltà massimo resta comunque sempre trascurabile (circa lo 0,4% sia per il premio a 8 anni che per quello a 16 anni). In Figura 3 rappresentiamo le stime relative alle distribuzioni di probabilità del premio fedeltà ad 8 anni (in alto a sinistra), e delle due componenti a scadenza. Come si nota, in tutti e tre i casi l’evento più probabile è avere un premio fedeltà pari al minimo garantito (0.4% del capitale investito alla scadenza dei primi 8 anni, e 0.6% più 1%, quindi l’1.6% del capitale investito a 16 anni), ma scenari più positivi per l’investitore “fedele” non sono eventi trascurabili.

Ipotizzando le cedole pari al valore minimo annunciato Venerdì 16 Aprile, consideriamo tre scenari:

Nel primo caso, valutando il titolo ai dati di mercato del 15 Aprile 2021 (curva dei tassi di interesse dei titoli di Stato italiani), il prezzo di mercato del titolo risulta essere pari a 102.12, quindi, a differenza del primo collocamento dei BTP futura, che era emesso alla pari, il valore del titolo è superiore al prezzo di emissione, come accaduto nella seconda emissione. Il tasso interno di rendimento del titolo (rendimento) è 1.38%, con il rendimento a 15 anni dei titoli di stato italiani ai dati di mercato di giovedì 15 Aprile posizionatosi intorno all’1.2%. Quindi il BTP futura – anche in assenza del premio fedeltà – avrà un rendimento superiore a quello di mercato di 18 punti base a differenza di quanto accadde nella prima emissione.

Nel secondo scenario il prezzo di mercato del titolo è pari a 103.81: l’investitore che compra questi titoli con la certezza di detenerli fino a scadenza li compra a sconto rispetto al loro valore effettivo. In questo caso il rendimento del titolo è pari a 1.49%. Il rendimento del titolo passa allo 1.71% nel caso di premi fedeltà massimi, scenario però poco probabile. Quindi il premio illiquidità connesso a detenere il titolo per sedici anni potrebbe arrivare a 50 punti base.

Possiamo quindi concludere che, se verranno confermate le cedole annunciate, il nuovo BTP Futura ha un rendimento leggermente superiore ad un classico BTP nel caso di assenza di premio di fedeltà. Il premio fedeltà corrisponde ad un aumento del rendimento di 29 punti base nel caso più probabile (premio fedeltà minimo).

The European Securities and Markets Authority (ESMA), the EU’s securities markets regulator,

today published its final report on the European Markets Infrastructure Regulations (EMIR) and

Securitised Financing Transactions Regulation (SFTR) data quality…

In line with the European Commission’s Request to the European Supervisory Authorities (ESAs) to periodically report on the cost and past performance of retail investment…

https://www.ivass.it/media/eiopa/documenti/2021/EIOPA_Cost_and_past_performance_report_2021.pdf

The Ontario Securities Commission (OSC) from Canada has approved four Ethereum Exchange Traded Funds (ETFs) to be launched on April 20, 2021…

https://www.newsbtc.com/news/ethereum-etf-approved-while-eth-gives-bullish-signals/

The price of Bitcoin suddenly dropped below $60,000 days after the Coinbase public listing…

https://cointelegraph.com/news/bitcoin-dips-under-60-000-what-s-pulling-down-btc-price

L’iniziativa di Finriskalert.it “Il termometro dei mercati finanziari” vuole presentare un indicatore settimanale sul grado di turbolenza/tensione dei mercati finanziari, con particolare attenzione all’Italia.

Significato degli indicatori

I colori sono assegnati in un’ottica VaR: se il valore riportato è superiore (inferiore) al quantile al 15%, il colore utilizzato è l’arancione. Se il valore riportato è superiore (inferiore) al quantile al 5% il colore utilizzato è il rosso. La banda (verso l’alto o verso il basso) viene selezionata, a seconda dell’indicatore, nella direzione dell’instabilità del mercato. I quantili vengono ricostruiti prendendo la serie storica di un anno di osservazioni: ad esempio, un valore in una casella rossa significa che appartiene al 5% dei valori meno positivi riscontrati nell’ultimo anno. Per le prime tre voci della sezione “Politica Monetaria”, le bande per definire il colore sono simmetriche (valori in positivo e in negativo). I dati riportati provengono dal database Thomson Reuters. Infine, la tendenza mostra la dinamica in atto e viene rappresentata dalle frecce: ↑,↓, ↔ indicano rispettivamente miglioramento, peggioramento, stabilità rispetto alla rilevazione precedente.

Disclaimer: Le informazioni contenute in questa pagina sono esclusivamente a scopo informativo e per uso personale. Le informazioni possono essere modificate da finriskalert.it in qualsiasi momento e senza preavviso. Finriskalert.it non può fornire alcuna garanzia in merito all’affidabilità, completezza, esattezza ed attualità dei dati riportati e, pertanto, non assume alcuna responsabilità per qualsiasi danno legato all’uso, proprio o improprio delle informazioni contenute in questa pagina. I contenuti presenti in questa pagina non devono in alcun modo essere intesi come consigli finanziari, economici, giuridici, fiscali o di altra natura e nessuna decisione d’investimento o qualsiasi altra decisione deve essere presa unicamente sulla base di questi dati.