The natural rate of interest, r* (or “r-star”), is defined as the real rate of interest that is neither expansionary nor contractionary…

Feb

07

2024

The natural rate of interest, r* (or “r-star”), is defined as the real rate of interest that is neither expansionary nor contractionary…

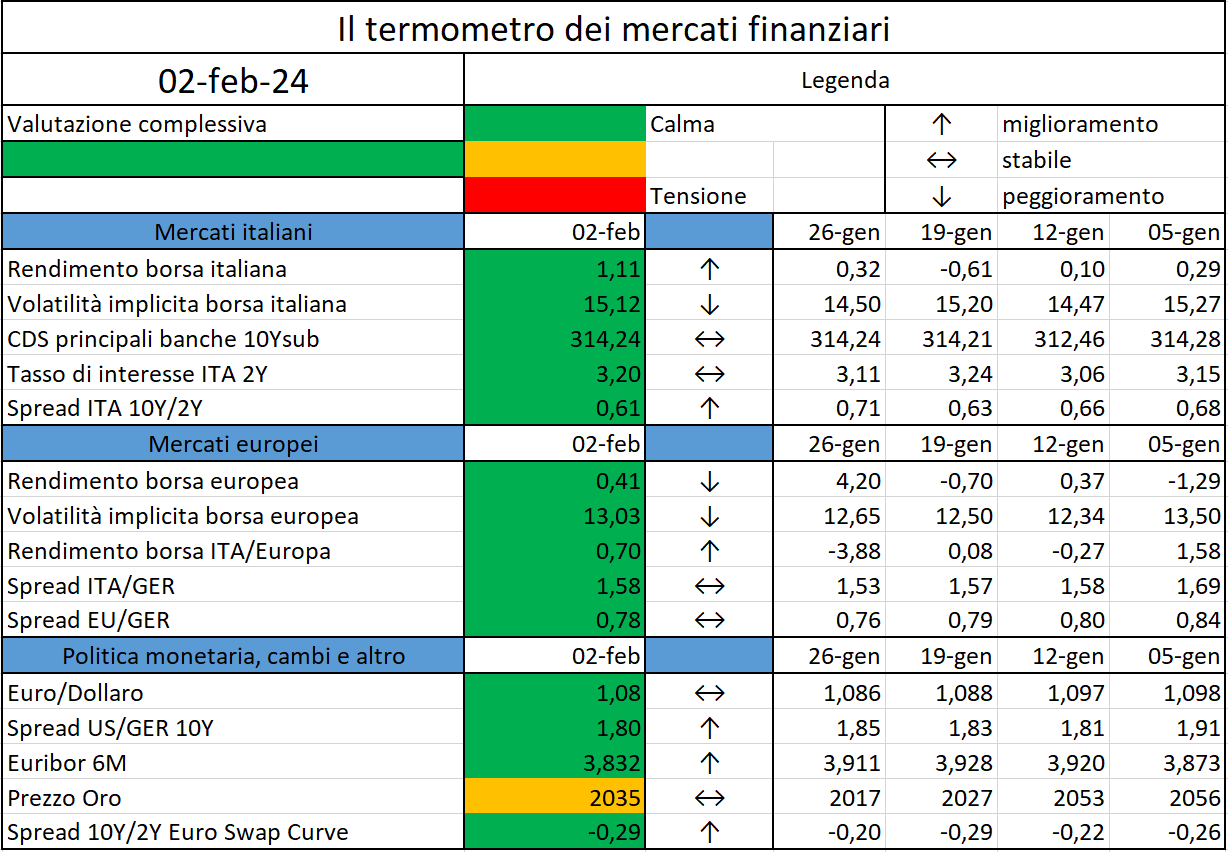

L’iniziativa di Finriskalert.it “Il termometro dei mercati finanziari” vuole presentare un indicatore settimanale sul grado di turbolenza/tensione dei mercati finanziari, con particolare attenzione all’Italia.

I colori sono assegnati in un’ottica VaR: se il valore riportato è superiore (inferiore) al quantile al 15%, il colore utilizzato è l’arancione. Se il valore riportato è superiore (inferiore) al quantile al 5% il colore utilizzato è il rosso. La banda (verso l’alto o verso il basso) viene selezionata, a seconda dell’indicatore, nella direzione dell’instabilità del mercato. I quantili vengono ricostruiti prendendo la serie storica di un anno di osservazioni: ad esempio, un valore in una casella rossa significa che appartiene al 5% dei valori meno positivi riscontrati nell’ultimo anno. Per le prime tre voci della sezione “Politica Monetaria”, le bande per definire il colore sono simmetriche (valori in positivo e in negativo). I dati riportati provengono dal database Thomson Reuters. Infine, la tendenza mostra la dinamica in atto e viene rappresentata dalle frecce: ↑,↓, ↔ indicano rispettivamente miglioramento, peggioramento, stabilità rispetto alla rilevazione precedente.

e Energy Information Administration (EIA), a statistics agency under the DOE, will survey the electricity use of selected U.S.-based miners over the coming six months starting next week, after putting out an “emergency collection of data request.”…

Overall credit terms and conditions offered to different counterparty types remained on balance unchanged between September and November 2023, contrasting with the expectations of further tightening expressed in the September 2023 survey…

https://www.ecb.europa.eu//press/pr/date/2024/html/ecb.pr240202~12b22c8c2b.en.html

The European Securities and Markets Authority (ESMA), the EU’s financial markets regulator and supervisor, has today published the new quarterly liquidity assessment of bonds, the data for the quarterly systematic internaliser calculations for equity, equity-like instruments, bonds and for other non-equity instruments and the consolidated tape provider (CTP) under MiFID II and MiFIR…

Il lavoro descrive il ruolo della moneta nell’economia e i canali attraverso cui l’introduzione di una moneta digitale emessa dalla banca centrale (central bank digital currency, CBDC) potrebbe influenzare il settore bancario…

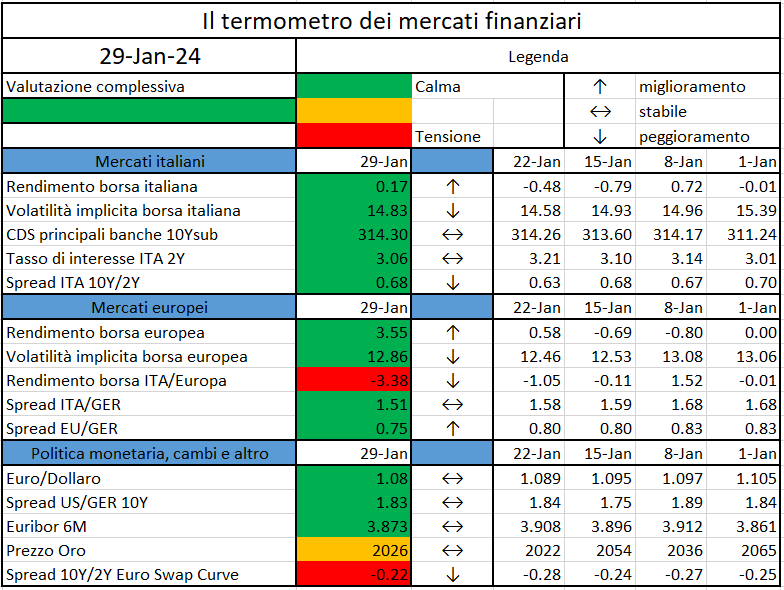

L’iniziativa di Finriskalert.it “Il termometro dei mercati finanziari” vuole presentare un indicatore settimanale sul grado di turbolenza/tensione dei mercati finanziari, con particolare attenzione all’Italia.

I colori sono assegnati in un’ottica VaR: se il valore riportato è superiore (inferiore) al quantile al 15%, il colore utilizzato è l’arancione. Se il valore riportato è superiore (inferiore) al quantile al 5% il colore utilizzato è il rosso. La banda (verso l’alto o verso il basso) viene selezionata, a seconda dell’indicatore, nella direzione dell’instabilità del mercato. I quantili vengono ricostruiti prendendo la serie storica di un anno di osservazioni: ad esempio, un valore in una casella rossa significa che appartiene al 5% dei valori meno positivi riscontrati nell’ultimo anno. Per le prime tre voci della sezione “Politica Monetaria”, le bande per definire il colore sono simmetriche (valori in positivo e in negativo). I dati riportati provengono dal database Thomson Reuters. Infine, la tendenza mostra la dinamica in atto e viene rappresentata dalle frecce: ↑,↓, ↔ indicano rispettivamente miglioramento, peggioramento, stabilità rispetto alla rilevazione precedente.

The European Securities and Markets Authority (ESMA), the EU’s financial markets regulator and supervisor, today published a report on the EU alternative investment funds (AIFs)’ market and an article on the risks posed by leveraged AIFs in the EU…

l Parlamento Europeo ha approvato lo scorso 10 gennaio la Direttiva proposta dalla Commissione, volta alla responsabilizzazione dei consumatori per la transizione verde, migliorando la tutela dalle pratiche sleali in materia di greenwashing…

https://www.dirittobancario.it/art/divieto-di-greenwashing-il-parlamento-ue-approva-la-direttiva/

On 18 December 2023 the Governing Council decided that recovery interest would be an appropriate corrective measure to propose to a national central bank (NCB)…

https://www.ecb.europa.eu//press/govcdec/otherdec/2024/html/ecb.gc240126~80908b06b4.en.html